Article • Dean Baker’s Beat the Press

That is what readers are asking after seeing an NYT article in which several economists expressed surprise over the continuing weakness of the economy. What is surprising in this picture? What sector did they expect to give a boost to the economy that fell short?

The special cues to the ignorance of the economists interviewed is the seeming surprise at the continuing drop in house prices. Do these economists still not know about the housing bubble? It almost crashed the financial system and is the cause of the current downturn. Can you actually get paid to be an economist and still not know about the bubble?

Of course if you knew about the bubble then you are not surprised that house prices are continuing to fall. Prices have to fall by about 10 percent in real terms to get back to their long-term trend. This means that the decline in house prices over the last half year should have been entirely predictable.

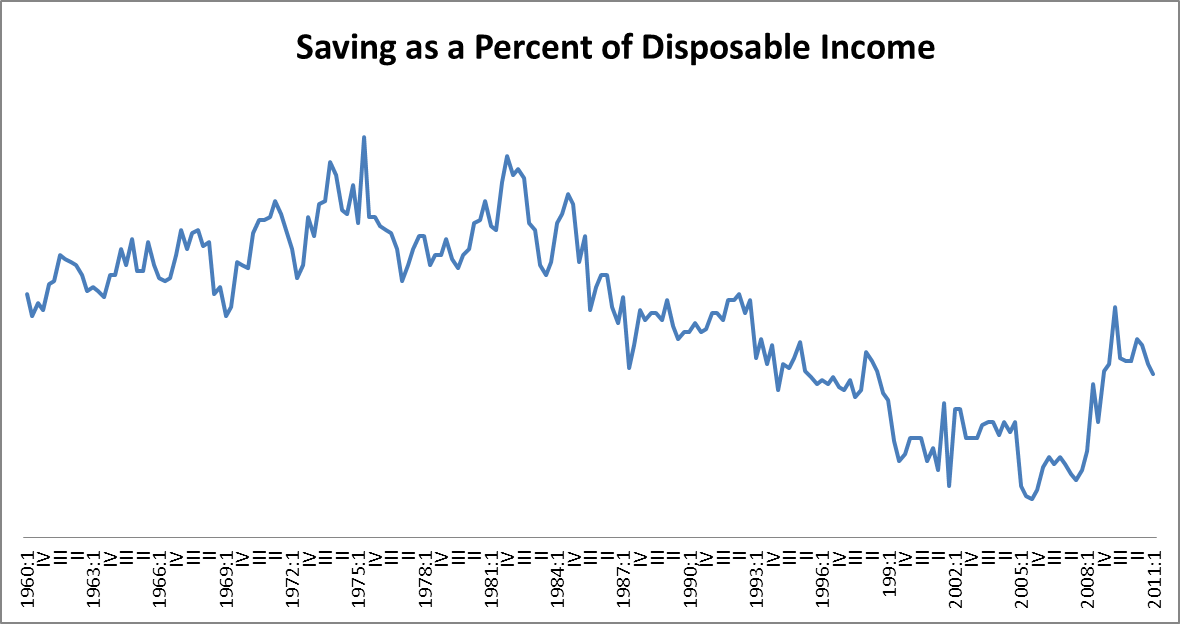

The economists cited in this article also seemed surprised that consumers aren’t spending more. Economists who know about the economy are the surprised that consumers are still spending as much as they are. The savings rate plummetted in the 90s and 00s as a result of the wealth created by the stock and housing bubbles. This is the result of the “wealth effect” whereby more wealth in assets leads to more consumption and less savings. This effect has been a central part of economics for more than 70 years.

With the housing bubble largely deflated, and the ephermal wealth that it created largely gone, savings rates are rising back to their historic level. If anything, the surprise is why consumption is so high, not why it is so low.

Source: Bureau of Economic Analysis. (Click here for a larger version.)

(Sorry about the mess of a graph — my Microsoft program was updated and in keeping with their proud tradition, the new version is much clumsier than then the old one.)