August 27, 2015

The stock market hovered at or near record highs throughout 2014, leading to high valuations for private equity-owned portfolio companies since prices for these companies are typically benchmarked to comparable publicly traded firms. With companies fetching high prices in this sellers’ market, PE funds were busy—in the words of Apollo chief Leon Black—selling everything that wasn’t nailed down. The result, according to PitchBook’s Benchmarking + Fund Performance report released yesterday, is that private equity funds returned a whopping $232.5 billion to pension funds and other limited partner investors last year.

According to PitchBook, private equity fundraising was highly successful in the first half of 2015 as investors counted up their winnings and recycled these gains into new PE funds. Unlike Donald Duck’s Uncle Scrooge sitting in his house counting up his money, however, pension funds and other private equity LPs are supposed to be sophisticated investors able to compare the returns from investing in private equity to other, less risky investment strategies. So, how do returns from investments in private equity compare with similar investments in the Russell 3000 stock market index? PitchBook conveniently provides that information as well.

As finance professionals know, the internal rate of return (IRR) is a poor indicator of financial performance. It is an algorithm that is subject to all manner of distortions. For example, when a successful portfolio company is sold at a high price yielding a high return early in the 10-year life of a PE fund, and the gains are distributed to the limited partners, the IRR algorithm assumes that the limited partners are able to reinvest these gains at the same high rate of return, something that is not actually possible. This leads to a very high IRR for the fund, but does not provide useful information on how investors in the fund really fared. It leads PE funds to sell high performers early, whether or not this is in the best interest of the funds’ investors. And it leads PE funds to require portfolio companies to sell junk bonds in order to finance a rich dividend payment to investors soon after the companies are acquired. These moves artificially raise the funds’ IRR, but may not be in the best interest of the funds’ investors.

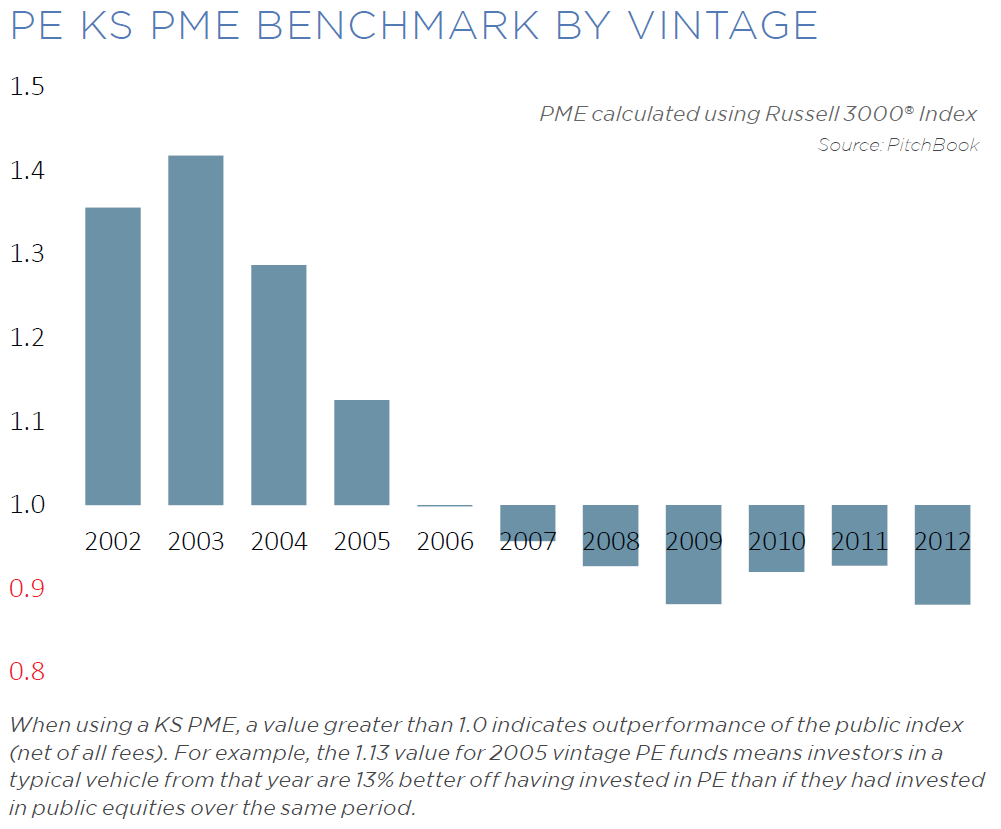

This problem was addressed a decade ago by two leading finance professors, Stanley Kaplan at the University of Chicago and Antoinette Schoar at MIT. They proposed a more accurate measure of actual returns received by pension funds and other limited partner investors which compares private equity returns with returns to investments in the stock market. The measure is known as the public market equivalent or PME, and is widely used by academics for benchmarking private equity returns against stock market returns.

Using the PME to measure returns to investors in private equity paints a very different picture of how investors fared. Low interest rates bailed out PE funds facing a wall of debt from leveraged buyouts of overpriced target companies during the bubble years preceding the financial crisis by making it easy for them to refinance this debt. The high flying stock market of 2013 and 2014 let PE funds unload these overpriced companies without having to take losses. Despite this, however, most PE funds launched in the last decade have failed to beat the market. The 2005 vintage is the last in which the median PE fund outperformed the stock market. Pension funds that invest in private equity are looking for returns at least 300 basis points above the stock market in order to justify the greater risk and illiquid nature of investments in PE. As can be seen in the graph below, despite near record payouts by private equity funds in the past two years, most pension funds have not seen these kinds of returns.

The current volatility in the stock market makes pricing companies held in private equity fund portfolios a challenging exercise. But even the sellers’ market for companies and the M&A boom of the past two years didn’t enable PE funds to outperform safer, liquid investments in the stock market. We are left with the puzzling question of why pension funds and other LP investors are so easily bedazzled by PE fund distributions and are ploughing these inferior gains back into private equity.