November 05, 2019

One of the tasks that are keeping economists employed these days is explaining the drop in labor’s share of Gross Domestic Product (GDP). This is supposed to be a major cause of concern since the vast majority of people get most or all of their income from working.

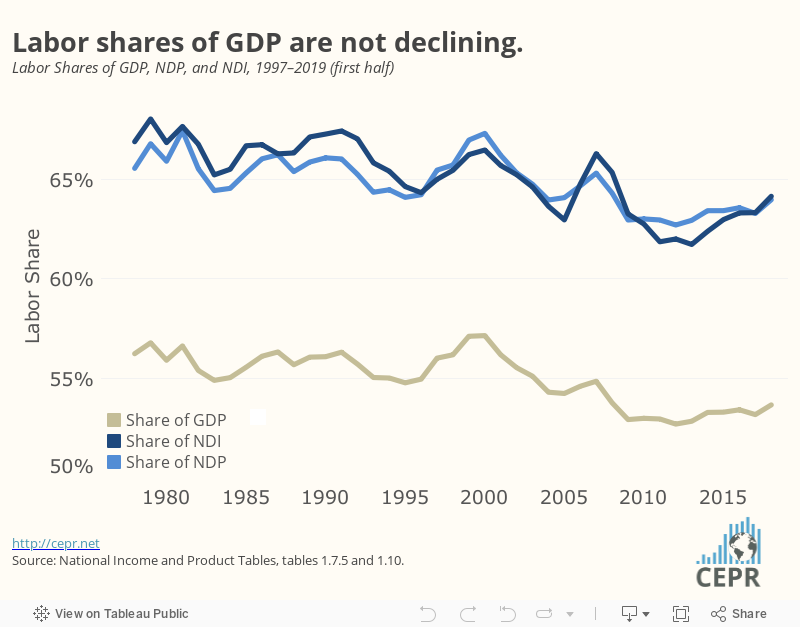

A wide variety of theories have been put forward to explain the decline. However, there is a big problem these theories; it is not clear that there has been much of a drop in the labor share.

Much of the decline in shares, before recent revisions, was simply due to an increase in the share of depreciation in GDP. Depreciation is the portion of output that is needed to replace worn-out capital. This is output that is neither profit nor wages; but the greater the depreciation share, other things being equal, the lower will be the labor share.

Revisions to data have lessened the impact of depreciation, but if we look at the drop in the labor share of GDP over the four decades from 1979 to 2019, it is 2.6 percentage points, as shown in Figure 1.

It’s not clear that this would be all that much to get excited over. The implication is that if the labor share had remained unchanged over this period, wages would be 4.8 percent higher. That’s not trivial, but clearly not the major cause of wage stagnation over this period.

However, if we look at the change in the labor share of Net Domestic Product (NDP) there is even less to be concerned over. The labor share of NDP fell by 1.6 percentage points over this forty-year period. If shares had remained unchanged, wages would be on average 2.5 percent higher today. Again, that would be good news, but hardly an earth-shaking change.

But there is something striking in the labor share of both GDP and NDP over the last four years. Despite low unemployment and rising real wages, there has been virtually no change in the labor share. It turns out that this is, in large part, due to the shrinkage in the size of the statistical discrepancy, the gap between GDP measured as output and the income side of the GDP measure. (In principle, these should be equal.)

If we look at the labor share of Net Domestic Income (NDI), it has risen by 2.4 percentage points over the last four-and-a-half years. While this still leaves the labor share 2.7 percentage points below its 1979 share (the labor share of NDI fell by more than the share of GDP or NDP), it does support the idea that labor is regaining lost ground at a healthy pace.

While we cannot be certain that the recovery will continue and wage growth remains reasonably strong, the fact is that the labor share usually increases in a recession. Profits fall much more than total output. This means that if the economy remains healthy, the labor share is likely to continue to increase due to rising wages, and if it falls into a recession, it is likely to rise due to falling profits. Either way, it does not look like we will have much of a story of falling labor shares.

This doesn’t mean that workers have nothing to complain about. Wages for most workers have badly lagged productivity growth over the last four decades. But the shift from labor to capital has been a relatively small part of the story. Most of the gap between the growth rate of productivity and the growth in the median wage is due to the rapid growth in the pay of the workers at and near the top of the wage distribution.

The pay of the typical worker has been depressed, in part, due to the growth in the pay of high-end professionals, like doctors and dentists, and especially very highly paid workers like Wall Street traders, CEOs, and hedge fund and private equity partners. These were the big winners in the economy over the last four decades. The shift from labor to capital is, by comparison, a minor sidebar.