February 03, 2021

The author would like to thank Eileen Appelbaum, Dean Baker, and Shawn Fremstad for their helpful comments, as well as Karen Conner for editorial assistance.

In Part I of this series, we addressed two of the immediate needs facing the Federal Government: cash assistance to individuals, and to state and local governments. Here in Part II, we confine our discussion to public investment, narrowly defined. What could be called public consumption is beyond our scope, not because it is unimportant — quite the contrary — but to keep the range of subject matter here more manageable.

The recession of 2020–2021 and the COVID-19 pandemic certainly concentrate the mind, but the longer-term needs of the nation deserve attention as well. In one sense, the concerns are complementary. An economic downturn is an ideal time to commence a prolonged period of new public investment. The spending boost is valuable in the short-term, and the reduced level of interest rates usually prevailing in a downturn makes long-term investment less costly.

The US government is ideally situated in the latter respect. What is called the real interest rate–the observed market rate for risk-free Federal bonds, minus the rate of expected inflation–is near zero. As John Quiggin points out, this means that to be profitable, an investment project need only defray its direct costs, without regard to debt service. In short, the economic conditions for a new wave of public investment could not be better.

Profit and cost in this context are not meant in the narrow accounting sense that a business firm would employ. We mean the social benefits of expenditure (which cannot fully be measured by reference to market prices) are at least equal to its costs in terms of actual utilization of resources. Such determinations may be difficult to arrive at, but the information used in such analyses properly informs decision-making. Moreover, considerations of equity should also figure into the evaluation of benefits and costs.

In this paper we first detail trends in public investment in conventional terms. In public discussion, investment is often reduced to infrastructure – roads, bridges, rail systems, and structures. There is indeed a need in these fields, but we don’t want to narrow consideration to them. Such investment is often associated, unnecessarily, with so-called male jobs.

In popular discussions, the term investment is distinguished from consumption and is often deployed by advocates to describe nondefense spending that may be meritorious but does not really satisfy a legitimate definition of investment.

Investment for our purposes is spending that generates numerous jobs in the immediate period in which the investment is undertaken and yields benefits far into the future. Investment may be viewed as fiscally prudent, while consumption conjures up programs that may be viewed by some as wasteful. But in actuality it is easy to think of genuine investments that are bad, such as the famous “bridge to nowhere,” and consumption spending that is well regarded, such as public health insurance for children.

We want to broaden consideration beyond traditional conceptions of investment to include the pressing need for investment in our care infrastructure, an infrastructure of care. By this we mean trained caregivers for children, the elderly, the disabled, the mentally ill, children without parents or guardians, victims of human trafficking, and beleaguered immigrants.

Education and training clearly fall into our definition of investment. For this paper, however, the relevant angle is the training of workers to operate care-oriented facilities or provide care services. Otherwise, elaboration of education investment, as far as the nation’s students are concerned, is beyond the scope of this paper. It should be noted that public schools may also provide care services. In fact, they are logical locations for the expansion of such services.

In one respect we wish to depart from the usual message. Rather than think in terms of a Green New Deal, we prefer to think in terms of a New Deal that is Green. Without question, public spending ought to pass through a filter reflecting the urgency of action to reverse climate change. But from a political standpoint, especially under current circumstances, the worries of the public at large are not centered around climate.

Noam Chomsky and Robert Pollin quote one of the “Yellow Jacket” protesters in in Climate Crisis and the Global Green New Deal, regarding proposals of French President Macron to raise the tax on gasoline: “[Y]ou are talking about the end of the world, but we are concerned with the end of the month. How are we to survive your reforms?”

The diverse working class needs and would favor a New Deal. The world needs a campaign to reverse global warming. The latter arguably depends on the former. Without assurances of economic security, the public will never support green policies.

It is quite possible to design a New Deal that seriously takes climate change into account. The words Green New Deal are just a label that could be retained, providing the associated campaign effectively conveys an overarching assurance of economic security for families.

It is not possible in a paper of this length to lay out a complete menu of worthwhile public investment. At any rate, any such program will be overwhelmingly informed by politics. There is no lack of candidates for investment. The much simpler message here, with several criteria in mind, is to do everything.

Critics of public investment usually discount its benefits to the public and the economy, while advocates often defend investment, the Green New Deal (GND), or care expenditure as a source of job creation. Both sides to this debate gloss over the economic benefits at stake.

Rejection of the possibility of benefits usually disguises an underlying animus, even on the part of those who would themselves benefit, towards receiving such benefits in common with others. Racial, gender, and class bias are often in play. Wealthier families may have little need for some public services.

On the advocate side, a basic confusion about macroeconomic policy is common. The Federal government can create all the jobs it chooses to using fiscal and monetary policy. The constraints on such policy are political, not economic. The jobs created need not be for investment, be green, be devoted to care, or even be at all productive or useful. Keynes spoke of hiring men to dig holes and fill them up again, to dramatize the potential for employment expansion.

In Part I we discussed the politically driven tendency to underestimate the potential for employment growth. Insofar as there is usually some slack in the economy (underutilized labor and capital), it is true that green policies can create jobs. However, so can non-green policies. In either case, as discussed in Part I, an economic downturn is an ideal moment to commence a new wave of public investment, another way to find opportunity in a crisis.

It is a commonplace that the traditional sort of infrastructure benefits business firms, profits, and GDP. Insofar as such investment is conditioned on reducing carbon emissions, it also contributes to economic security in the future through avoidance of the dangers inherent in climate change. However, there is no particular impact on employment or GDP in the present that could not be obtained by public spending without regard to climate change.

The key point about green investment is that it does not reduce employment or GDP. Nor need it detract from economic security in the present. It changes the composition of GDP and employment, especially for the benefit of future generations.

An investment whose benefits exceed its costs may or may not increase GDP in the future, since some or all the benefit may not be realized in any market transaction. For accounting purposes, we might want to set a price on carbon emission reduction, but that would be a matter of fiat, not a precise one tangibly resulting from any economic analysis of benefits.

Below we discuss the economics of a care infrastructure at a bit more length.

As noted above, existing nondefense public investment is concentrated in roads, bridges, rail systems, and structures. (The structures are primarily school buildings.) These are tangible assets, what could be included under a rubric of physical public capital or fixed assets. The vast bulk are operated under the auspices of state and local governments, in which they are said to reside. In 2019, for instance, the stock of nondefense fixed assets under the purview of the Federal government was under $2 trillion, while the states had over $12 trillion.

Roads. A commitment to combating climate change suggests that the current and traditional emphasis on roads ought to be reduced, but there are countervailing considerations. One is that it will be some time before Americans surrender their automobiles. In the meantime, for the sake of road safety and economical car maintenance, roads need to be kept in a state of good repair.

Second, road maintenance is an appealing resort during a downturn, since it provides a plethora of shovel-ready projects that do not require lead time devoted to extensive planning, environmental assessment, and other preparation.

Third, social transit includes buses, and of course buses need roads. The same could be said of most bicycle travel. Fourth, there are limits to the extent that rail systems can be expanded. And fifth, the construction of new rail systems of any type takes decades, and climate change requires more timely action. The more immediate option to fulfill social transit needs is expanded bus service. Better broadband coverage, publicly provided where necessary, would facilitate telework and reduce the need for transit.

Bridges. When the Interstate 35W bridge over the Mississippi River in downtown Minneapolis collapsed in 2007, it was a major event. The reality is that such failures are also rare events. There are hundreds of thousands of bridges in the US in assorted states of upkeep. When a bridge has deteriorated to the extent where it can no longer be fully used, access to it is routinely restricted for safety’s sake. Most bridges classified as in need of maintenance are still in use and are invariably not at risk of major failure. All the same, there is much maintenance work that could be done, also of the shovel-ready variety.

The Federal Government provides grants for transportation, but these moneys typically do not fund major new capital projects. There aren’t enough funds for such purposes. To begin with, the grant money is spread too thinly to support any individual state’s big-ticket endeavors. Moreover, roads get the lion’s share of new funding. Big new capital projects are usually financed by Federal earmarks and have the benefit of subsidized borrowing by state and local governments.

Bridges could be thought of as climate neutral. They are needed by all forms of surface transportation. It would be possible to prioritize bridges devoted to rail and bicycle, though it would require the cooperation of state and local governments.

Rail. The two types of rail are intercity and intraregional. There has been a clamor for high-speed rail for the US, where passenger rail service seriously lags that of other nations in terms of speed, cost, convenience, and comfort. An additional benefit of intercity rail is that, for certain routes, it can displace a significant amount of air travel. The latter is a greater generator of carbon emissions.

The dilemma for the US is that for the rail route most likely to be successful – the East Coast from Boston to Florida – the density of existing construction, particularly around major cities, makes the acquisition and placement of high-speed rail lines inordinately difficult. Furthermore, the planning required for new lines pushes the date of actual construction and eventual operation well into the future. The need for action against climate change is more imminent.

An exception is the California High-Speed Rail System (CHSRS), for which planning, land acquisition, and construction have already begun. Ample funding for this system has yet to be established. If fully built-out, the project could link Sacramento to San Diego and accomplish several things.

First, it would be a proof of concept to encourage the construction of such systems elsewhere in the US. Besides the East Coast corridor, the other major candidate would be a Midwest network centered over Chicago.

Second, it would provide economic development to the impoverished Central Valley of California.

Third, it would eliminate much of the Los Angeles to San Francisco air travel and intercity automobile travel, aligning with our concern about climate change. While the benefits of the system would be substantially confined to California, the larger objectives qualify the CHSRS as a project of national significance, justifying Federal support.

From an equity standpoint, a shortcoming of intercity rail is that it primarily serves business and leisure travel. If it were a choice between intercity and regional rail system investment, the latter would better serve the needs of working-class commuters and shoppers. It would link workers isolated in suburbs to jobs in the cities and provide options to low-income shoppers stuck in inner city food deserts. Another factor weighing against it, as noted above, is the very long lead time for the completion of new systems, relative to the urgency of immediate action on climate change.

In metropolitan regions, including economically depressed neighborhoods, expansion of rail and bus systems could provide invaluable economic revival. Indeed, the sad history of roadbuilding inspired by urban renewal was responsible for the plight of such neighborhoods in the first place.

Rail systems would generally be run by state and local governments, possibly in a regional compact. As discussed in Part I of this series, these governments are currently in no position to undertake major capital projects. To push the CHSR project over the top, as well as to expand regional systems, a new Federal commitment is required. Moreover, the maintenance and operations costs of such systems are a major responsibility that will not be defrayed by ticket revenues. Few passenger rail systems in the world are funded solely by ticket sales. A continuing Federal role will be required.

There is no reason the US cannot have first-class intercity and regional rail systems. We address cost considerations in the next installment of this series.

Structures. The case for school repair, especially in the heat of the current pandemic, is manifest. On top of bricks and mortar we could include the increased use of broadband. Naturally, construction design and upgrade ought to be configured to preclude structures’ contribution to carbon emissions.

Here again, the overwhelming bulk of capital assets are under the purview of thousands of municipal governments and school districts. This complicates the distribution of grants-in-aid for purposes of maintenance and new construction.

In keeping with an interest in caregiving, school construction should proceed to expand capacity for preschool and childcare services. If community college is to be made more accessible under reduced or eliminated tuition fees, construction for that expansion may also be needed. Corollary requirements for such objectives are resources for training of personnel to operate such facilities.

One crisis that is not quite visible is the state of provisions for long-term care. At present the nation lacks both the facilities to care for the wave of baby boom elderly who will be unable to care for themselves, as well as any viable insurance options for those who will need care. Related populations with some overlap are the homeless and the long-term, persistently unemployed.

On the surface, these would seem to be problems of providing adequate housing, supplemented for some with assisted living services, though one should not forget about worker training for those needed to operate new facilities.

In the same vein, we argue that immigration, legal and otherwise, could be understood simply as a problem of transitional housing. Broadly speaking, immigrants make for a larger economy. Over the long term, they should be no less productive than native-born citizens. The nation has always been able to absorb refugees from different cultures, and the job market has always expanded to accommodate them. The economic problem boils down to putting decent roofs over their heads in the short term until they can integrate themselves into the economy. Of course, the politics are a different matter.

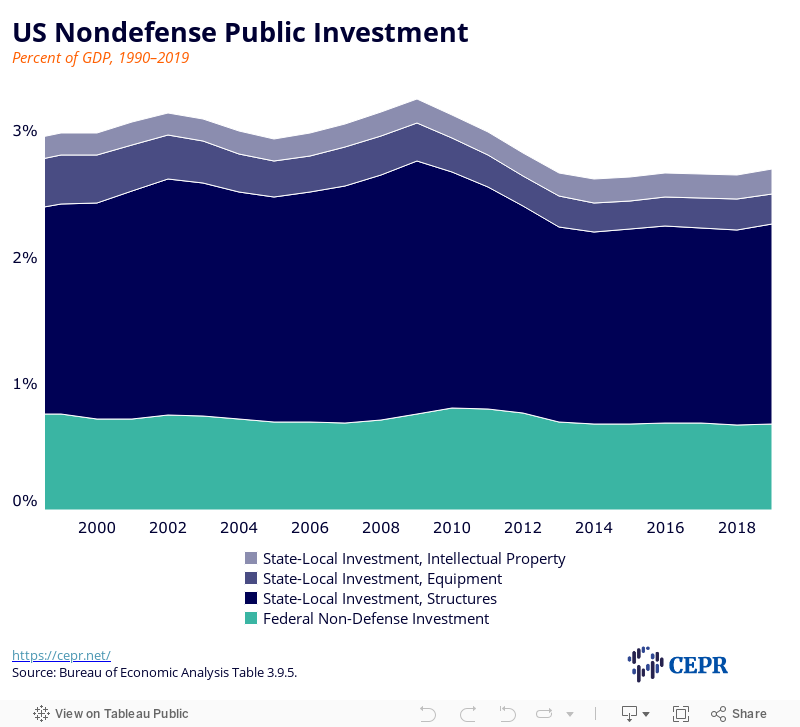

Figure 1

Figure 1 shows the major categories of public investment since 1990 as shares of GDP: Federal defense, Federal nondefense, and state and local. Given totals of roughly three percent of GDP, a single percentage point in this category of public spending means a lot.

Over the entire time frame, notwithstanding the bracketing of four terms of Democratic presidents, there is no secular growth in the total share of GDP devoted to public investment. In fact, the principal growth in the period, from 2000 to 2008, was during the presidency of George W. Bush. Moreover, from the depths of the Great Recession in 2009, total nondefense investment sustained a further drop.

From 1990 to 2000, the final two years of the presidency of George H.W. Bush and both terms of Bill Clinton, a substantial build-down of the defense budget was accomplished. By 2000, defense investment was roughly a full percentage point of GDP less than in 1990. As noted above, this was not reprogrammed into nondefense investment. The ramp-up after 9/11 was rolled back, presumably why President Trump claimed the Army was “out of bullets.”

If there was a commitment to counter-recessionary policy, it would have shown up in a rise in the proportions following the trough years (1991, 2001, 2009) in Figure 1. It is in such periods that pressure on the state-local sector in particular is greatest. No such reaction is evident.

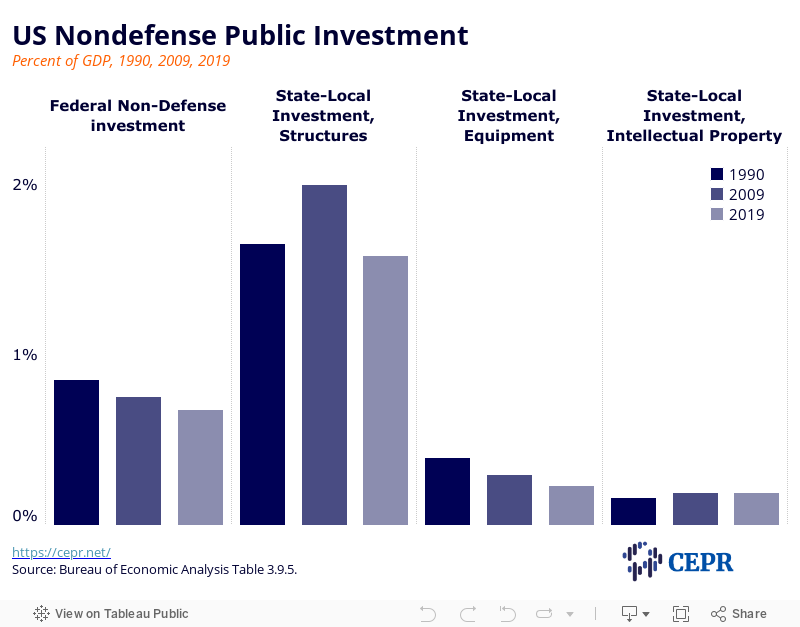

Figure 2

Figure 2 shows the same data as Figure 1, but in a different form. We chose the peak year of 2009 to illustrate very long-term changes in investment since 1990. As noted above, a percentage point of GDP means a lot, especially for subcategories. There is decline in Federal nondefense investment and state-local investment in equipment, and little change in state-local IP investment. (IP is short for intellectual property and refers to software and general research and development.) State-local investment in structures peaks in 2009 but then falls back to prior levels.

In Table 1, adapted from the Department of Commerce version, we provide a more detailed breakdown of the state and local government component, again with respect to GDP, along with the major Federal categories for purposes of comparison.

Gauging nondefense investment relative to GDP makes sense as an indicator of need. A larger economy needs more public and private capital goods to function. Defense needs would logically depend on the costs of preparation for real or potential threats. We elaborate on the defense budget in the next installment in this series.

| (billions of dollars) | |

|---|---|

| Government Fixed Assets (1) | 289.7 |

| Equipment | 86.6 |

| Structures | 112.0 |

| Intellectual property products | 91.1 |

| Federal | 157.6 |

| National defense | 107.3 |

| Nondefense | 50.2 |

| Equipment | 8.1 |

| Structures | 7.4 |

| Intellectual property products | 34.8 |

| State and local | 132.2 |

| Equipment | 23.9 |

| Structures | 98.5 |

| Residential | 3.4 |

| Office | 7.1 |

| Commercial | 0.3 |

| Health care | 2.5 |

| Educational | 16.3 |

| Public safety | 4.6 |

| Amusement and recreation | 3.1 |

| Transportation | 7.7 |

| Power | 3.3 |

| Highways and streets | 33.0 |

| Sewer systems | 9.1 |

| Water systems | 6.3 |

| Conservation and development | 1.6 |

| Other structures (2) | 0.3 |

| Intellectual property products | 9.7 |

| Software | 4.8 |

| Research and development | 4.9 |

Source and Notes: Bureau of Economic Analysis Table 7.1.

1. Consists of the fixed assets of general government and government enterprises.

2. Consists of lodging, communication, and manufacturing.

As noted above, roads are the biggest investment category, with educational structures next in magnitude. Rail systems fall under the transportation category. There is no data separating training expenses undertaken by state and local governments. Nor is there any indication of investment devoted to what we have categorized as care. The closest candidate is health care, which clearly applies to a broader class of functions than those we have specified for caregiving.

Our general conclusion is that there has been little expansion of nondefense public investment in the US for decades.

By care we mean services for the sustenance of populations unable to care for themselves, including children, the indigent elderly, the disabled, the homeless, victims of human or labor trafficking, elderly in need of long-term care, and beleaguered immigrants.

Unfortunately, there isn’t much in the way of official data on the physical components of our care infrastructure. There is much more data on the needs side. A useful overview is here.

In general, the paucity of data mirrors the barren commitment of the country to those in need of care. The Biden Administration addresses this problem with a plan to devote resources to childcare, long-term care, and the related functions noted previously.

The targets of this plan are well-taken. A question will be adequacy. The Biden administration’s campaign language repeated a commitment to ensuring access, but providing access is not the same as guaranteeing it to all comers. If the supply of a service is limited, access is not equivalent to universal provision.

In this paper, our treatment of what could be called the care infrastructure is limited by the focus on tangible investment. It abstracts from the system of law and regulation that would underly benefits provided to those in need. The benefits themselves, however well-taken, would ordinarily be thought of as consumption, not investment.

The economics of care are not confined to the direct services provided. For example, consider the needs of children, elderly, and those otherwise incapable of caring for themselves. Care must be provided either in the home or in an institutional setting. We have already noted that such care ought to be provided by trained personnel. The training and the bricks and mortar for institutions are all a matter of investment. They provide services in the future.

But the service itself provides additional economic benefits. As noted above, it is not merely a matter of employment levels. The availability of caregivers makes possible the paid employment of family members otherwise drafted into caregiving and unable to participate in the workforce. For instance, a parent staying at home, obliged to do a job that a trained day care worker could do, might otherwise be able to hold a higher-productivity jobs outside the home, raising GDP, not to mention their own income.

Care arrangements, whether in the home or elsewhere, would be expected to reduce the resort of workers to unplanned sick days or personal days. Broadly speaking, the expanded availability of care would permit the fuller participation of workers in general and women in particular in paid employment. Workers would establish more consistent work records, to the mutual benefit of themselves, their employers, and the national economy.

In some circumstances, institutional care might be less desirable than home care – more costly and less appealing. The elderly and disabled might prefer noninstitutional care, while parents might prefer institutional care for their children. Institutional care could be a particular problem in rural areas that lack the population density to support large, high quality facilities. Presently, the Medicaid program is biased against home care, a problem that will interest the new Administration.

The dual crises of COVID-19 and the economic collapse are relevant here. COVID-19 makes some institutional settings for care problematic due to the difficulties of practicing social distancing. The economic collapse has torn through small businesses and nonprofits that might otherwise be contracted with to provide care services. Both point to the importance of direct public provision of care services in institutional settings, and the need for enough wisdom and flexibility to support home-based alternatives. Finally, the dominance of state and local governments in the provision of what care services are available in the US returns us to the problem of their own dire fiscal circumstances, discussed in Part I of this series.

In recent years there has been an upsurge of interest in the problem of monopoly – the domination of entire industries by single firms. From the standpoint of textbook definitions of economic efficiency, monopoly fails because such firms set prices higher than marginal cost, resulting in insufficient output of the product or service in question. The typical critique of monopoly, including from liberals, points to the merits of a more competitive market, which means the benefits of increasing the number of suppliers by breaking up the monopoly firms. What is usually understated, if not missing altogether in these treatments, is the alternative of social ownership.

From an economic standpoint, there is no principled basis to prefer multiple suppliers to a single, public enterprise. The latter need not be required to maximize profits. A public enterprise can be permitted to sustain accounting losses for the sake of charging efficient prices that reflect the marginal costs of production.

To be sure, in some cases it could be more beneficial to pursue a competitive market supplied by private, for-profit business firms. The current, liberal interest in antitrust commits the logical error of ruling out the social ownership alternative. The difficult answer to whether antitrust or social ownership is preferable is, it depends.

Expanding the scope of public sector enterprise is not at the forefront of public attention, but if we are speaking of public investment, acquiring and organizing the assets needed for new public enterprises is certainly a form of investment. In a previous report, we elaborated on one case that has garnered some public attention: the US Postal Service (USPS), as arguably a pillar of US communications infrastructure. The history of the service in the US could be seen as a history of lost opportunities to expand the scope of public sector output.

The USPS, originally the Post Office Department (POD), was in on the ground floor of the telegraph, which it was obliged to surrender to the private sector. It heavily subsidized the formation of rail systems and air transport and might have carved out an ownership share of these industries in their infancy.

In other countries, the postal service operations go well beyond the delivery of mail and packages. In the United Kingdom, postal banking survives, as it once did in the US. In France, Le Poste also operated telephone and telegraph services until they were privatized in 1991. Le Poste still operates a bank and insurance company, a logistics service company, and a mobile telephone service. In Argentina, the government is preparing to set up a counterpart to Amazon under the purview of its own postal service.

The logic of antitrust — breaking up big companies — does not easily apply easily to the chief targets of such discussion today, mainly Amazon, Facebook, Google, and Twitter. In the case of Amazon, it is possible to imagine certain separate components, such as Amazon Kindle books or Amazon Web Services.

The dilemma is that replacing one big monopoly with multiple, separate monopolies is not necessarily an improvement. This problem arises in the case of social media, whose value is precisely in its networked, monopolistic command of its market. It would not make sense to have Facebook New York, Facebook New Jersey, etc.

Serious thought has been given to seeking a viable competition policy in these cases, and we do not mean to reject any such work out of hand. Our only reservation is that public alternatives ought to be included in the considerations. The multiple harms wrought by untethered tech monopolies, in terms of fomenting perverse social messages, violating basic norms of personal privacy, and gross mistreatment of their own employees, have been a national scandal.

Hopefully, the remedies that will be sought will not be biased in favor of efforts towards competition, rather than public replacement. As a Boston Globe editorial suggests, “[A] new kind of social media platform must be funded by public and philanthropic sources, in a financing model akin to that of public broadcasting.” (We should note that hopes for public broadcasting being sustained entirely by public financing have not panned out.)

The establishment of new public enterprises is especially relevant to reverse climate change and, as noted elsewhere in this paper, care services. As far as the GND is concerned, carbon emissions and assorted types of environmental pollution have been understood as problems of taxation, the construction of new markets (e.g., tradable pollution permits), or regulation. There is not much disagreement that such efforts have come too little thus far. Despite dilatory action in the US, the world is still looking at a deadline to control carbon emissions, lest a tipping point be breached beyond which global warming would proceed unchecked, with disastrous consequences.

We have to assume that, to date, products enabling the greening of the economy have yet to be profitable from a business standpoint. (Solar panels are an exception. The obstacles to their proliferation lie in the incentives to convert to solar, and to the regulatory obstacles erected by utility companies.) Otherwise, we would see a cornucopia of such output.

The profit constraint that private investors demand and business firms must observe fails to account for the unmarketable public benefits of green tech, described by economists as externalities. Public enterprises would not be thus constrained.

Of course, a public agency can waste money. But there is no foundation in economic theory for the premise that a public enterprise must cover its costs with revenue from user fees or other revenues directly charged to customers.

The history of the post office provides a case in point. The Post Office Department (USPS, after 1971) nourished economic development in the nation and employed subsidies for the delivery of mail and packages, technically running unprofitable lines of business for its entire history.1

The US Federal system is composed of 50 sovereign states and a handful of territories. It includes over 90,000 local governments: counties, municipalities, cities, school districts, townships, special districts, and Indian tribes.

Sub-Federal Governments are obliged to maintain balanced budgets. This requirement is reflected in a variety of legal provisions, but the underlying reason is economic. Insofar as state and local governments must sell bonds to private investors to raise money for capital projects, the interest rates they are able to charge depend on their reliability as borrowers.

The purchasers of these bonds, typically relatively sophisticated investors and financial firms, will demand returns commensurate with their assessment of the borrowers’ ability to carry debt. A state or local government in financial difficulty will be required to offer higher interest rates on bonds they sell. Accordingly, such governments must keep expenditures in line with revenues, as well as provide legal guarantees that bond repayment will be prioritized over other spending, even including basic public services.

Since the bulk of public capital assets resides in the state-local sector, the expansion of US public investment will depend primarily on increased Federal aid to the states. It follows that the Green New Deal will as well.

Before addressing direct Federal aid, we note two tax-based sources of Federal aid to states. We also address the role of capital budgeting in state and local finance.

Deduction for state and local income and property tax (SALT). Taxpayers who itemize deductions on the Federal income tax may deduct income, sales, and property taxes paid to their state and local governments. This deduction was capped at $10,000 by Trump’s Tax Cuts and Jobs Act, starting in 2019. The deduction implies a discount on state taxes. The beneficiaries are primarily higher-income persons, so as far as the tax side goes, there is little dispute that the deduction is regressive. That is, it benefits higher income people more than lower-income persons.

Such criticism fails to reckon with the public spending effect, and who may benefit from it. The deduction subsidizes state and local revenue collections, in essence by granting wealthier taxpayers a discount on their state and local taxes. In this way it provides some boost to state and local government spending, whose beneficiaries may be found at every income level.

A fair analysis of the equity of the tax provision would take into account the spending effects. Income and property taxes are the greatest source of state and local revenues, so the SALT deduction also constitutes Federal support for public investment in the state-local sector. In fiscal year 2020, the SALT deduction cost the Federal Government $13.4 billion.

Exemption of interest on state and local government bonds. A taxpayer receiving interest from the purchase of bonds sold by state and local governments is able to exclude such interest from his or her taxable income. This reduces the burden of borrowing costs on state and local governments, since they are able to sell bonds at a somewhat reduced interest rate. The purchaser of the bond is willing to accept the reduced rate because the interest income from the bond is tax-exempt in the Federal income tax. Deductibility keeps the bonds competitive with other investments of similar risk.

Here again, there is an implicit Federal subsidy to state and local governments, this one particularly affecting capital projects. Bonds in practice and in some cases by law are limited to the finance of investment, not current consumption expenditure. This deduction cost the Federal Government $24.6 billion in FY 2020.

Like the SALT deduction, the exemption of bond interest is also focused on high income persons. But in this case as well, the full distributive effect properly includes the consequences for state spending; in the case of bonds, spending for capital projects. A common textbook criticism of both provisions is that the cost to the Federal Government would be reduced and improved from the standpoint of equity if the aid instead took the form of direct grants.

The shortcoming of this reasoning is that such resources are not easily translated in that manner. The aid in the first place owes its political existence to the ancillary benefits to third parties; in this case, higher-income taxpayers. There are many examples in US public finance of political support by well-off third parties for one or another sort of public expenditure or tax benefit ostensibly aimed at the middle-class or the poor. The superiority of financing measures stripped of any subsidies to third parties is theoretical, not practical.

Capital budgeting. States’ balanced budget requirements raise the question of capital budgeting practices by state and local governments.

When a government or a business of any size purchases a durable physical asset, it need not be booked as a current expenditure or cost. An asset by definition generates a stream of benefits in the future. Under capital budgeting, it is only the depreciation of the asset that is counted as a current cost in annual accounts.

Capital budgets are ubiquitous in state and local finance, but they are strictly limited to accounting for capital projects. Lenders like to see projects whose benefits can be monetized, such as tolls for a bridge or highway. Such proceeds then provide a natural basis for servicing the debts associated with financing the facility.

Capital budgeting practices are strictly excluded from Federal budget accounting, as well as from scoring (the estimate of costs) by the Congressional Budget Office of new legislative proposals. This creates an implicit bias against Federal investment relative to consumption.

An additional problem for investment planned with Green New Deal priorities in mind is that not all the returns, or perhaps none of the returns, can be monetized by reference to market transactions. This also makes benefit-cost analysis and the investment decisions it is intended to inform difficult. The California High-Speed Rail System provides a case in point.

The CHSRS should reduce air travel, particularly between San Francisco and Los Angeles. This would reduce carbon emissions and airport congestion. It would reduce auto travel, easing the trip for those still making it by car. We could imagine less air pollution for the same reasons, with a positive impact on health. These are just a few of the details that would require pricing to determine the total social benefits of the CHSRS. Naturally, it would not do to charge travelers for the entirety of such benefits, since much of them are enjoyed by those who do not use the system.

Ordinarily in a budget, the income generated by an asset is classified as revenue, but much of the in-go for GND investment is not monetized. So, capital budgeting is of little use. Moreover, the absence of tangible revenue streams obviates private sector finance of GND projects, unless there is some kind of Federal subsidy or guarantee.

We turn now to the most direct sort of Federal subsidy to state and local budgets: grants-in-aid.

Table 2 shows Federal grants for physical capital investment. The total for FY2020 (which runs from October 2019 through September 2020) was $87.3 billion. As noted above, contemporaneous tax-based assistance was about $38 billion (though the SALT deduction facilitates state and local spending of all types). A translation of the SALT benefit into grants would be a significant boost to the states’ resources, political practicalities cited previously aside.

| Fiscal Year | Grants for Physical Capital | Grants for Physical Capital | Portion of total Grants | Grants for Physical Capital Share of State and Local Gross Investment |

|---|---|---|---|---|

| (billions, dollars) | (2020 dollars) | (percent) | (percent) | |

| 1990 | 27.2 | 48.4 | 20.1 | 21.0 |

| 2000 | 48.7 | 70.8 | 17.0 | 21.3 |

| 2005 | 60.8 | 78.8 | 14.2 | 21.2 |

| 2010 | 93.3 | 110.4 | 15.3 | 26.8 |

| 2015 | 77.2 | 83.8 | 12.4 | 21.8 |

| 2019 | 80.8 | 81.7 | 11.2 | 19.4 |

| 2020 | 87.3 | 87.3 | 11.0 |

Source and Notes: Budget of the US Government, FY2021, Analytical Perspectives Volume, Table 14-1.

Note the years shown are not evenly spaced, so inference of consistent trends from these data would be misleading. One fact that sticks out is aid of this type stagnated after 2005, aside from a rise in the second year of Obama’s term when the Democrats retained control of both houses of Congress. Another is the steady decline in the share of total grants since 1990 due in part to the rise in Medicaid expenditures. Third, is that the extent of Federal leverage exhibits the same pattern as total grants adjusted for inflation — a rise and fall between 2005 and 2015 — but is otherwise roughly the same 21 percent.

The lack of enthusiasm among Democrats for grants to state and local governments is a political problem for GND investment through the state and local sector, aside from the general opposition of Republicans to nondefense spending of all types. Grants facilitate the self-glorification of state and local politicians who are blessed with the privilege of spending the money, and the vilification of Congress and the President, who bear the burden of raising taxes to finance said aid. An individual member of Congress can take credit for an earmark that finances the construction of a new facility. They can attend the ribbon cutting. Political credit for a Federal grant supported by the entire Congress tends to be spread much more thinly.

In more recent years, the opposition of conservative state governments has placed a further obstacle in the way of Federal policy. In some cases, even when Federal funding amounted to a virtual free lunch to state governments, it was rejected for ideological reasons. Examples include the Medicaid program and the heavily subsidized Medicaid extensions under the Affordable Care Act.

The institution of new public enterprises creates a different sort of opportunity. In the context of this paper, they would be Federally sponsored. The components of such new investment projects can be geographically located in keeping with additional objectives. For instance, new enterprises dedicated to manufacturing products, let’s say zero-carbon emission buses, could be located in states in desperate need of economic development. For decades, private sector defense contractors made such decisions out of political considerations.

The scope of US public investment should be broadened in the direction of new public enterprises such as postal banking and the care economy.

The benefits of public investment in the framework of a Green New Deal, as well as the care infrastructure, will be real but not entirely observed in the form of a higher measured GDP.

Green investment and expansion of care services are often motivated as employment-generating, and this is true for conditions of less than full employment. Otherwise, they change the composition of employment and GDP, not its level. Green investment and care spending that close employment gaps may expand GDP in future years. The bulk of resources for a US public investment boom in keeping with a Green New Deal, and for an expanded care infrastructure, must be provided to state and local governments. Naturally, their participation will have to extend to planning and design, and not be confined to administering national plans. It will be a daunting task, but public policy in a very large economy under a Federal system of government has always been so.

Addonizio, Michael, “America’s schools are crumbling. What will it take to fix them?” The Conversation, March 5, 2019. https://theconversation.com/americas-schools-are-crumbling-what-will-it-take-to-fix-them-111720

Cebul, Brent, “Tearing Down Black America,” The Boston Review, July 22, 2020. http://bostonreview.net/race/brent-cebul-tearing-down-black-america

Chomsky, Noam and Robert Pollin, with C. J. Polychroniou, Climate Crisis and the Global Green New Deal, Verso, 2020.

Gleckman, Howard, “End Medicaid’s Institutional Bias for Long-Term Care,” Forbes, September 25, 2013. https://www.forbes.com/sites/howardgleckman/2013/09/25/end-medicaids-institutional-bias-for-long-term-care/?sh=7446173763e0

Kalipeni, Josephine, and Julie Kashen, “Building Our Care Infrastructure,” Caring Across Generations, September 1, 2020. https://caringacross.org/wp-content/uploads/2020/09/Building-Our-Care-infrastructure_FINAL.pdf

Putnam, Bradley, Danish Iqbal, and Matt Acconciamessa, “The Food Desert Predictor,” MIDS Capstone Project, Summer 2017, University of California/Berkeley. https://www.ischool.berkeley.edu/projects/2017/food-desert-predictor

Quiggin, John, “Why zero interest rates are here to stay,” The Conversation, November 11, 2020. https://theconversation.com/why-zero-interest-rates-are-here-to-stay-149523

Rikap, Cecilia, “What would a state-owned Amazon look like? Ask Argentina,” Open Democracy, November 24, 2020. https://www.opendemocracy.net/en/oureconomy/what-would-state-owned-amazon-look-ask-argentina/

Office of Management and Budget. Budget of the United States Government, 2021: Analytical Perspectives. January 2020. https://www.govinfo.gov/content/pkg/BUDGET-2021-PER/pdf/BUDGET-2021-PER.pdf

Sawicky, Max B., “Save the States,” Center for Economic and Policy Research, March 31, 2020. https://cepr.net/save-the-states/

Sawicky, Max B., “The US Postal Service Is a National Asset. Don’t Trash It,” Center for Economic and Policy Research, September 2020. https://www.cepr.net/wp-content/uploads/2020/09/2020-09-USPS-Sawicky.pdf

Sawicky, Max B. “How to Make Joe Biden’s Budget Better: Send Money Now!” Center for Economic and Policy Research, January 11, 2021. https://www.cepr.net/wp-content/uploads/2021/01/2021-01-Federal-Budget-Sawicky-1.pdf

Teachout, Zephyr, “How Biden Can Break the Stranglehold of Amazon and Other Monopolies,” The Nation, January 4, 2021. https://www.thenation.com/article/economy/monopoly-policy-biden/

U.S. Census Bureau, 2017 Census of Governments–Organization. https://www.census.gov/data/tables/2017/econ/gus/2017-governments.html

U.S. Government Accountability Office. Budget Issues: State Balanced Budget Practices, AFMD-86-22BR, December 10, 1985. https://www.gao.gov/products/AFMD-86-22BR

U.S. Government Accountability Office. Highway Bridge Program: Clearer Goals and Performance Measures Needed for a More Focused and Sustainable Program, GAO-08-1127T, September 10, 2008. https://www.gao.gov/products/GAO-08-1127T

U.S. Government Accountability Office. California High-Speed Passenger Rail: Project Estimates Could Be Improved to Better Inform Decisions, GAO-13-304, March 28, 2013. https://www.gao.gov/products/GAO-13-304