March 11, 2021

The author would like to thank Eileen Appelbaum, Dean Baker, and Shawn Fremstad for their helpful comments, as well as Karen Conner and Sarah Rawlins for editorial assistance.

In Parts I and II of this series we have declared a great need and capacity for additional Federal spending, putting aside the question of financing. In public debates, any sort of proposal for nondefense spending immediately draws the “How do you pay for it” question. In the past, it has been asserted that any spending proposal should be accompanied with ‘pay-for’ provisions. In the same way, under rules of procedure, legislation for new spending in the current Congress has been similarly encumbered.

As a political matter, the constraint of included financing tends to dampen consideration of worthwhile spending initiatives. It has long been noted that similar constraints are applied unequally, if at all, to defense spending or tax cuts.

From the advocate’s standpoint, a more sensible political practice is to win support for spending on its own merits and leave the debate over financing for later. The accumulated history of conservative hypocrisy over the national debt makes the task easier. In actual policy making, however, somehow or other, sooner or later, the piper must be paid. Several routes are available.

The variety of potential financing mechanisms should further relax or at least delay any political need for attaching financing provisions to spending proposals. Furthermore, in the context of the Federal budget as a whole, attaching specific financing to each separate item on an extended menu of new spending would be foolish. It is the aggregate of new spending that would determine financing mechanisms.

This paper focuses on the three most likely ways to pay for new spending: cuts in defense spending, tax increases, and borrowing (deficit spending). By way of background, we try to establish the relevance of a popular new topic in budget debates, the so-called Modern Monetary Theory (MMT).

For spending growth, we discuss three different scenarios.

Scenario I: Federal spending expands enough to get the economy out of the current recession, and back to levels analogous to the GDP at the end of 2019.

Scenario II: The Federal spending level expands significantly beyond the level suggested by the first scenario, to a new, higher normal, but not far out of line with recent experience, after which it tracks GDP growth.

Scenario III: The final scenario considers what it would take for the US to achieve a public sector comparable to those in Europe. These systems are commonly referred to as social democratic or democratic socialism. (To this writer, for all practical purposes, there is no meaningful difference.)

Our conclusion regarding the latter, admittedly a very ambitious scenario, is that a Green New Deal (GND) cannot be accomplished without it. A Green New Deal requires a New Deal that is green, and a New Deal that is green (which includes, among other things, universal health insurance coverage) requires a transition to social democracy.

The past 10 years have seen the popularization of an economic doctrine known as Modern Monetary Theory (MMT). With others, we like to stipulate a distinction between MMT as economic theory and MMT as political rhetoric.

MMT as Economics. The MMT school of economic theory is descended from followers of John Maynard Keynes. These scholars formed a community that described itself as post-Keynesian. Leading exponents included Abba Lerner, Hyman Minsky, Wynne Godley, and Paul Davidson. They distinguished themselves from the more dominant views in the economics profession, typified by such figures as Paul Samuelson, or today, Paul Krugman and Larry Summers.

This is not an economic treatise, so we will not attempt to explicate MMT theory at any length. Briefly, according to this school, the economy often operates below its potential, meaning at less than full employment. In that circumstance, the US Federal government can spend the economy to full employment without making offsetting changes in taxes and without resort to borrowing. In other words, the government can simply write checks (informally understood as “printing money”) for new spending that it desires. The binding constraint is not the public debt, but the possibility of inflation if the government expands spending by too much.

MMT is broadly faithful to the older post-Keynesian tradition, which is why it is sometimes described as offering nothing new. The fairness of this charge is beyond the scope of this paper. What should be understood is that MMT is a legitimate body of theory upheld by eminent economists. A comprehensive textbook treatment is here. A new, popular treatment is here.

One of the infamous claims of MMT is that the US government, because it is a sovereign entity that uses its own currency, cannot go bankrupt. Debts can always be paid by writing checks – printing more money. Ironically, while this may sound like the old joke, “How can I be broke? I still have more checks!” it is the least controversial of MMT precepts, conceded by economists holding a wide variety of views. More to the point is what might be inferred from that fact.

MMT Rhetoric. The most provocative claim of MMT is that taxes do not finance spending. The implication for the naïve is that Federal spending is unlimited. We can have all the nice things we want, unencumbered by the political burden of associating new spending with higher taxes. An example of a breathless take on this can be found in Aaron Wistar’s review of The Deficit Myth, the best-selling book elaborating MMT theory by Professor Stephanie Kelton, “Medicare for All? We can afford it. A multi-trillion-dollar Green New Deal? We can afford it. A guaranteed job for anyone who wants to work? That, too. And, Kelton argues, we don’t necessarily need to raise taxes to do all this.”

The image of an unlimited source of funding for liberal projects has understandably tempted advocates whose proposals have been routinely confounded by concerns, some hypocritical and others not, about budget deficits.

Sloppy, not to say dishonest, criticism of MMT claims that its understanding would lead to ruinous inflation, citing such cases as Zimbabwe or Weimar Germany. Actual MMT doctrine is that if the Federal government writes too many checks (e.g., “prints” too much money), causing a spike in the price level, it can drain purchasing power from the economy with taxes, and the Federal Reserve can cool down inflation by raising interest rates. A tax increase offsets the boost to spending. Undesirable inflation is further precluded by the interest rate hikes.

Broadly speaking, the inflation rap on MMT is the same sort of attack leveled at liberal economics of all types for the past 50 years, if not longer. Deficit spending and growing public debt have been said to cause interest rates and inflation to explode. Past episodes of increased deficits do not bear this out.

In a certain literal, superficial sense, taxes indeed do not literally finance spending. However, we should also say that at some point, spending requires some response in the form of taxation, borrowing, and/or monetary policy. It may not be dollar-for-dollar, but some kind of balance – acknowledged in MMT theory – must be established for inflation to remain at acceptable levels.

Can “money printing” alone ever bring forth greater public spending without the danger of inflation? Often it can, since the economy frequently operates with some amount of “slack,” which means that not all resources and labor are fully employed. But there are limits to the maximum output and employment that can be achieved. As discussed in Part I, these limits are usually understated for political reasons. But limits there are, so at full employment, if the price level is locked down, more public spending means less private spending. If the price level is not locked down, more public spending raises the price level.

There is no limitless cornucopia of resources for new progressive projects. This should be particularly obvious when the economy is at full employment. To get more of anything, we have to accept less of something else. We cannot help but think the dramatic MMT assertion that taxes do not finance spending is a distinction without a difference. This writer sees the claim as more appropriate to political rhetoric than to theory.

We find much MMT public rhetoric by pundits to be misleading, a kind of bait and switch. The bait is that unlimited public spending, without the political burden of “pay-fors,” is possible. The switch is the belated admission that additional spending, at some point, can put upward pressure on the price level and require a response. The obvious response would be higher taxes and contractionary monetary policy, but MMT writers discount the likelihood or merits of taxation in favor of alternative measures.

The alternatives include, roughly in descending order of desirability, deferred compensation, moderation of wage demands, price controls, and “patriotic savings.”2

Deferred compensation may sound like an easy lift, since it would be repaid with interest, much like a traditional IRA. However, if the GND takes years to implement, compensation is likely to be deferred for some time. Moderation of wage demands is less appealing. A wage increase foregone this year reduces the worker’s base for future increases. In the same vein, to some extent price controls will trickle down to labor compensation.

Nobody likes taxes. Taxes to arrest inflation would have to bear most heavily on consumption, and on the unrich, since that is the source of most purchasing in the economy. The political appeal of the alternatives to taxes is left to the judgment of the reader. They could be uncharitably described as consumption repression by other means.

The constructive crux of MMT is that usually, fiscal and monetary activism can significantly expand the horizons of Federal spending without the risk of inflation or spikes in interest rates. That is reflected in Scenario I proposed at the beginning of this paper, and was demonstrated in 2020, which saw a Federal budget deficit of $3.3 trillion (up from $984 billion in 2019)3 and no serious signs of inflation. An economic downturn such as the current one enhances the possibilities for deficit-financed spending growth.

Deficit reduction mania used to seize Democrats, even more than Republicans, to their political sorrow. Since 1970, we have had two or perhaps three cycles where Democratic presidents exercised spending restraint, followed by electoral defeats for their Congressional allies. Republicans dined out on proclamations of allegiance to fiscal frugality, while Democrats bore the brunt of the blame. When the Republicans came to power, no such reservations on deficit spending were put in place.

It has taken several decades, but by now the Democrats have wised up to this scam, in two crucial respects. One is that they are less willing to be suckered into austerity policy, with the understanding that their efforts will later be unceremoniously undone by Republicans in the form of new tax cuts and defense spending increases. Two is that past experience has finally attenuated fears of deficit increases during economic downturns. As noted previously, the predicted interest rate spikes and hyperinflation never came to pass.

What remains to be seen is how Democrats regard the longer-term condition of Social Security and Medicare. As things stand, the payroll tax revenue dedicated to these programs is projected to run short of scheduled benefits. For Social Security, that point is 2034. For Medicare, it is 2026. At those times, by law, benefits would have to be reduced. A willingness to countenance deficits during the current downturn is not equivalent to a willingness to provide those programs with all the revenue they will need to maintain promised benefits in the future.

The bright side of the picture is that there is a broad consensus favoring a substantial ramp-up in nondefense, deficit spending for the time being. In this paper, however, we are trying to think big. So even granting the economic feasibility of much higher deficits, along the lines of Scenarios I and II, we would like to push further to consider how even larger increases in public spending in keeping with Scenario III can be accommodated by some degree of offset, in the form of reductions in defense spending and tax increases. In other words, how could the US finance a transition to a social democratic public sector?

In past analyses of the Federal budget, it was common for economists to defer to others when it came to the question of defense spending. The presumption was that it was not necessary to be an expert on housing, environmental protection, or health care, for instance, to pontificate on those subjects. However, national security was supposed to be plagued by overarching complexity.

Presumably, in a democratic society, the people are entitled to a voice on all matters. We need not defer to self-selected national security experts whose track records have, to put it mildly, met with less than brilliant success. A dilemma for progressive critics is that authority tends to be vested in those with government experience, and government experience tends to accrue to those in accord with established views, however vulnerable to criticism those views might be.

Current spending on defense and nuclear weapons (the latter under the auspices of the Department of Energy) exceeds levels during the Korean War, the Vietnam War, or the Reagan build-up in the 1980s. US nuclear capability was primarily motivated by a parallel build-up in the Soviet Union. The Vietnam debacle was often justified by reference to the domino theory: that through Vietnam, Chinese communism would spread to the rest of Southeast Asia.

It came to pass that the Peoples Republic of China (PRC) actually waged war against their purported brethren in Vietnam. Later still, the PRC became a capitalist juggernaut and one of our biggest trade partners, while Vietnam hosted Nike factories. The dissolution of the USSR and the US failure in Vietnam and, more recently, the Middle East ought to provoke a reevaluation of the extent and nature of actual threats to US national security.

Relying on common sense, as well as consultations with experts, we choose to highlight the following principal sources of savings in the field of defense spending:

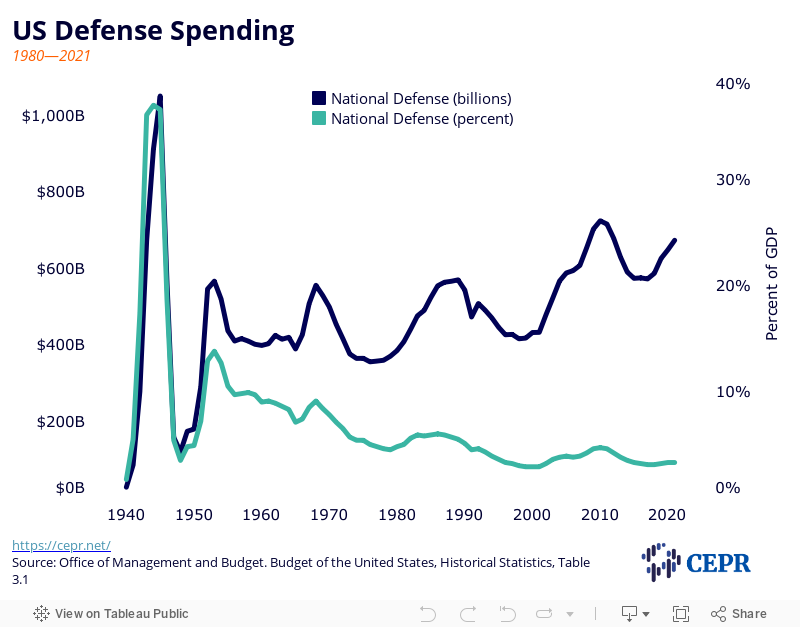

In Figure 1, defense spending is illustrated in two forms. The blue line is spending adjusted for inflation. The orange line is spending as a share of GDP. Each way of measuring spending has different implications.

Spending in constant dollars reflects the trend in the use of real resources. The share of GDP reflects the extent of foregone output of other types that might have been produced, under different circumstances, in relative terms. Since 1954 (the year after the end of the Korean War), economic growth has steadily reduced the sacrifice of alternative goods and services, relative to GDP. At the same time, spending adjusted for inflation has been growing since 1977.

This defense category in budget accounting does not include outlays that might easily be classified as part of national security. Most obvious are the separate accounts for the Department of Homeland Security and the Department of Veterans Affairs. The defense numbers shown here are thus biased downward.

We’ve suggested that, broadly speaking, the extent of public and private nondefense investment ought to keep pace with economic growth. A growing economy requires more of the public capital goods, like infrastructure, that the private sector will not provide. Defense spending is arguably different. It is reasonable to suggest that a larger GDP means the nation can afford more defense spending, but the need for defense spending logically depends on the nature of threats to US national security.

Shrinkage of Personnel. Since World War II, the dominant doctrine in US military thinking was that the nation needed to be prepared to fight major land wars involving tens of thousands of troops, or “boots on the ground.” As recently as 2018, the Department of Defense designated the intentions of Russia and China as threats to US national security, though the pressure of their policies is borne for the most part, in both cases, by their immediate neighborhoods – nations bordering Russia, and for China, the East and Southeast Asian regions.

Is the prosecution of a major land war in either of these two theaters a plausible endeavor? Common sense suggests not, for at least two different reasons. When it comes to Europe, the EU nations’ economic power dwarfs that of Russia. By rights, they should be able to defend themselves. It’s not difficult to imagine Russia bullying its immediate neighbors, as it has already with Ukraine. Is it possible, or wise, to imagine the US going to war in defense of Ukraine or, say, any of the Baltic nations?

The case of China is even less believable. Without doubt, China’s economy has grown to a scale to rival that of the US After the debacle in Vietnam, however, is it at all possible to imagine the US engaging the immense Chinese military on the ground in Asia? Chinese expansionism is predominantly economic, not military. As far as territory goes, its chief interests have been limited to its immediate neighborhood, especially Hong Kong and Taiwan, which it regards as parts of China proper.

Recent debacles in Iraq, Libya, and the “endless war” in Afghanistan reduce the justification for new adventures in that part of the world. A sad example is the ongoing carnage in Yemen, underwritten until very recently by the U.S. taxpayer.

Where does all that leave the case for maintaining 800 military bases around the world, supporting the capability of fighting a major land war? Where could such a war possibly take place? US policy has been dedicated to employing enough resources to maintain an overwhelmingly dominant “overmatch” military position – a very large hammer looking for a very big nail, in a world with a few little nails.

The role of ground troops would seem to be limited to small-scale, specialized operations aimed at terrorists or the rescue of threatened populations. The greatest defense savings are to be found in shrinking the forces now in place in readiness for imaginary, major land wars.

One likely target for termination is the so-called Overseas Contingency Operations (OCO) account, used to fund ongoing military action, that has been criticized for functioning as a slush fund.

Reduction of Nuclear Arsenal. As spending goes, in terms of bang for the buck, nuclear weapons are relatively cheap. It still follows that the extent of the nation’s nuclear arsenal is far in excess of any conceivable need, and moreover, this arsenal could be reduced by mutual agreement with Russia. Reviving Obama’s agreement with Iran, reneged on by Trump, serves that objective as well. Arms limitation initiatives were completely abandoned during the Trump Administration. Resumption could bring budget savings. The savings under this scenario would not be trivial – perhaps a trillion dollars over 10 years.

Reduced Privatization. The Department of Defense (DOD) employs some 600,000 contractors. Notwithstanding hopes of exploiting the efficiency of the private sector, well over a third of contracting does not follow competitive procedures (e.g., organizing competitive bidding on contracts). Moreover, even in the use of competitive bidding, selection criteria have been found to be vague. (Spoiler alert: the lowest bid doesn’t necessarily get the job.) And finally, while defense contracting employs incentives to encourage better contractor performance, the DOD does not know if these incentives work.

The overarching DOD scandal is the reality, acknowledged by conservatives, that their budget reporting has been rife with inaccuracy for years. Indeed, in their own documents, DOD needs to assure us that “The Department will continue its plan to achieve full auditability of all its operations.”

To be fair, it is not clear if results would be any better if work were done in-house. Those unable to manage contracting may not be able to manage actual production any better. It seems more likely that a reduced budget and removal of a profit constraint would exert internal pressure for greater efficiency.

Sand in the gears of the revolving door could wear down the collaboration between the DOD and the corporate sector. One lever that has inflated the costs of defense contracting has been the corruption of the legislative process due to the machinations of lobbyists. Rules limiting the passage of Federal officials into the corporate sector and back again could be beneficial.

While the case for defense cuts may seem strong, performing the cuts will take time. Big-ticket hardware contracts tend to have multiyear time spans and cannot be unwound instantly. DOD employees will need transitional assistance to private sector jobs. Nobody is going to reduce veterans’ benefits; the savings in that vein will come from having fewer wars, a smaller number of personnel in uniform, and fewer veterans in the future.

Taxes finance spending, but they have other uses as well. Taxes can alter the distribution of income in the direction of greater or lesser equality. They can also be designed to encourage or discourage designated types of behavior. In practice, specific tax sources may be dedicated to particular categories of spending.

There is broad agreement that, at least for the immediate future, additional taxes to offset deficit increases are not needed. However, if we allow ourselves to envision much larger increases in spending along the lines of Scenarios II or III, then the option of offsetting a proportion of such spending growth with higher taxes (or, following MMT, similar means) remains salient. As noted previously, at the point when the economy is running at full capacity, more of anything means less of something else.

The four principal available means to increase revenues are

Higher Rates. The greatest opportunity in this category lies in the individual income tax. Recent work suggests the top marginal rates could be much higher. Reference is often made to rates exceeding 90 percent in the 1950s, though those rates applied to relatively few people. Today, in the wake of sizable gains by those with the highest incomes even during the major economic downturn of 2020, increasing the top rate or adding additional tax brackets would bring in significant revenue. For instance, according to the Congressional Budget Office, raising the marginal rates for the top two brackets (e.g., taxable income in excess of $415,000 for married couples filing jointly in 2020) by just 1 percentage point (from 35 to 36, and from 37 to 38) would increase revenues by $114 billion over 10 years. Rates of 70 percent or more have been suggested. That’s a lot of elbow room to raise rates.

The second major source of Federal revenue is the payroll tax. In this case, a rate increase, while probably feasible in economic terms, would affect all wage earners, including those with the lowest pay. For that reason, alternatives to increase revenue are preferable. For instance, expansion of the payroll tax base on the high side, as previously noted, could eventually be used to fund Social Security and Medicare benefits.

The third most important revenue source is the corporate income tax (CIT). Much public debate points out that the US corporate rate is higher than that in other advanced industrial countries. These discussions often gloss over the reality that tax law permits deductions from profits to the point where many corporations earning billions in profits are able to erase any positive tax liability. The average CIT rate in the US, sometimes called the “effective rate,” is not out of line with rates in other nations. When compared to GDP, US corporate tax revenue is very low compared to other nations.

Tax Expenditures. News coverage of taxes tends to focus on marginal tax rates, while progressive advocacy tends to fixate on the top marginal rates. However, just as important is the admittedly more arcane question of how the tax base is defined. Deductions, credits, deferrals, and exclusions reduce the revenue productivity of any given rate or set of rates. Taxpayers with very high incomes can end up paying little or no tax; for them, the rates don’t matter.

Both the Office of Management and Budget and the Congressional Budget Office publish an annual accounting of tax expenditures which refers to the revenue costs of particular features of the Federal tax code. For progressive advocates that view these as a virtual shopping list, here are several cautionary remarks:

One, keep in mind that the whole is less than the sum of the parts. That is, the revenue estimates apply to each provision in isolation. When two or more provisions are considered together, some revenues attributed to them separately may overlap. The total from repeal will be less than the published sum of the items.

Two, some of the largest tax expenditures apply to a broad section of the upper middle-class. Politicians approach their repeal with trepidation. One recent exception discussed in Part II of this series is the state and local tax (SALT) expenditure for state and local governments, which was reduced in Donald Trump’s tax cut bill in 2017. Big middle-class tax expenditures are not politically invulnerable.

In the case of SALT, it is particularly beneficial to “blue states” that tend to rely more on their state individual income taxes and on higher taxes in general to provide the health care and social spending that common decency and their citizens deem necessary. The goal of the Trump administration was to drive down “blue state” spending on social programs to the level in “red states.”

The progressive dilemma in approaching tax expenditures such as SALT is the potentially regressive effect of the benefit. Eliminating it might, in isolation or with all “other things equal,” improve after-tax income equality, but other things are never equal. To accurately gauge the impact of repeal, the implications for Federal, state, and local budgets should be considered. For instance, the Federal government might use the proceeds of repeal for deficit reduction, for additional defense spending, or for some other, even less desirable tax cut. State and local governments might cover their loss by reducing social spending.

One category of tax expenditures ripe for elimination in light of climate change would be subsidies to oil and gas production. An obvious use for the funds would be GND expenditures. Unfortunately, the totality of these Federal tax breaks was less than $14 billion in Fiscal Year 2019, and much less if we maintain provisions aimed at conservation, clean energy, and the like. Others estimate an additional $5 or $6 billion in subsidies from state and local governments.4 Under any scenario, much more resources would be needed for a GND.

Another revenue source of interest is the Estate and Gift Tax. This is most important for concerns about inequality since the tax is only relevant to the richest taxpayers in the US. As noted above, these same taxpayers have enjoyed greater income gains than others. They have further benefitted from shrinkage of the Estate and Gift Tax base, which, besides touching only the largest estates, is also riddled with devices that enable the rich to remove any tax at all from their estates. In general, base broadening and enforcement are more pressing for this tax than rate increases.

Finally, there is the question of taxing wealth. Senator Elizabeth Warren made a war cry out of “two cents,” in reference to her proposal for a wealth tax rate of 2 percent. We should note that if the return to an asset is a modest 4 percent, a 2 percent wealth tax is a 50 percent tax on capital income. The point is simply that the rate of a proposed wealth tax can be deceptive.

A wealth tax would probably depress the prices of financial assets and encourage additional tax avoidance and evasion behavior by the wealthy. These are not disabling problems, but they do take some air out of the balloon. The most important effect of the tax is to reduce inequality, not to finance additional Federal spending.

Taxing Externalities. When parties engage in a market transaction, there can be good or bad effects on third parties. The classic example is pollution, and the classic remedy is to levy taxes on transactions that result in pollution. The tax discourages the activity, and the revenue might be used to remediate the costs of pollution.

Today the leading candidate for externality taxation in light of climate change is a tax on carbon or greenhouse gas emissions. The base for such taxes would be very large and potentially provide a great deal of revenue. The hope is that it would have a big, negative impact on emissions and finance GND spending initiatives. Since a wide range of products and services are a source of carbon emissions, such a tax would be roughly analogous to a sales tax in terms of its effect on income inequality. In other words, without any modifications, a carbon tax would be regressive.

One commonly suggested remedy is a rebate of part of the revenue, aimed at focusing its refund effect on those with lower incomes, which Paul, Fremstad, and Mason call a “carbon dividend.” It should be noted that even a flat universal basic income (UBI)-style rebate (fixed dollar amount to all) would provide greater tax relief, relative to income, to lower income households. Schemes that provide a stronger progressive impact would also be possible, at the cost of some complexity for taxpayers and for the Internal Revenue Service. (In Part I, we offered some criticism of UBI programs.)

Another popular target for externality taxation, especially in light of the news at the end of January 2021, is financial transactions. The traditional nostrum is that the stock market improves the allocation of capital by showing what companies are worth and which ones ought to expand or contract. It is well established, however, that most corporate investment is financed internally, not from sales of stock. The stock market is more like a casino than a source of objective assessments of optimal investment opportunities when it comes to real investment in plants, equipment, and training.

A great volume of financial market transactions, particularly in securities tied to home mortgages, was the root of the Great Recession of 2008. These were basically bets on the solvency of mortgage holders. When combined with a bubble in housing prices, the consequences were devastating for the world economy.

The social value of speculation in financial instruments of all types is elusive, to say the least. A tax on transactions would primarily affect those making the largest or most frequent transactions, typically the wealthy. The tax would have the wholesome effect of curbing such transactions, at least marginally, as well as providing revenue for useful public purposes. An estimate of the proceeds of such a tax, at a rate of 0.1 percent, is $752 billion over 10 years.

Another new idea – really an old idea that has been revived – is the proposal from former Rep. Beto O’Rourke (D-TX) for a “war tax.” In light of the past six decades of US military misadventures, O’Rourke and others reason that it is too easy for the president to employ military force. Under the Constitution, a declaration of war is supposed to be a prerogative of Congress. In practice, this constraint on presidential administrations has been effectively nullified.

Besides returning war powers back to Congress, an additional obstacle could be placed in front of war-making by requiring that proposed defense expenditures to enable new campaigns be accompanied by an additional, temporary tax. This would basically reverse the current, perverse situation where defense spending enjoys blank checks, and nondefense spending proposals are hounded by demands to propose new taxes or other means of paying for nondefense expenditures.

Beto suggested that the proceeds of his proposed war tax would be dedicated to veterans’ health services. In effect, a war tax protects any peace dividend wrung out of the defense budget that would be forthcoming under an enlightened foreign policy.

Enforcing Tax Law. On an irregular basis, the Internal Revenue Service publishes reports on the “tax gap” – the amount of additional revenues that would be collected if all taxpayers paid what they rightfully owed, on time. The failure to pay on time, or ever, is tax evasion, which is distinguished from tax avoidance. The latter is the legal resort to tax planning that reduces tax liability.

The extent of outright tax evasion is significant. Roughly one-in-six dollars of taxes owed is not paid in a timely fashion, by the most recent data. (Delays in paying taxes past the legal deadline is tantamount to tax evasion since the deferral of a legal liability could earn interest income. Time is money.)

For those wealthy persons with complex financial affairs, tax planning may approach, if not cross, the boundary between legality and fraud. Dealing with such cases is costly for the IRS, so it is obliged to employ what is known as an “offer in compromise.” Taxpayers have the opportunity to negotiate to pay less than what they legally owe, which means they can, in effect, be pardoned for what are described as “aggressive returns.”

Funding for the IRS has been increasingly inadequate for decades. Its first task, its core mission, is to process returns. Enforcement of tax law depends on whatever is left over. The incentive for the IRS is to surrender to requests for offers in compromise. The more legal and accounting firepower the taxpayer can bring to his or her application, the less able is the IRS to resist compromise.

The upshot is that an increase in resources to the IRS for tax administration would more than pay for itself. Unfortunately, by the rules of Congressional budget “scoring,” such expenditures are measured only in terms of out-go — the extra spending, with no account of in-go — the additional revenues that would be recovered.

Years ago, this author was assured by highly placed government economists that estimates of such savings were too difficult, or too uncertain to calculate, evidently in contrast to many other budget calculations that have been dogged by inaccuracy over the years. It turns out that economic science has now progressed to the point where estimates of the payoff for increased IRS spending can in fact be estimated, as illustrated in this CBO report in Option 31. Unfortunately, the rules for scoring have not changed. The scoring for IRS spending remains one-sided.

Seigniorage refers to the additional output that can be called from the economy, in times of economic slack, by nothing more than the Federal government writing checks for new spending — “printing money.” Seigniorage is a legitimate source of additional public spending. The extent of it depends on the state of the economy and the manner in which monetary policy is conducted.

One spectacular example of seigniorage was the “mint the coin” craze during the Obama Administration when the Republican Congress was obstructing Administration policies with debt ceilings. Apparently, it would have been perfectly legal for the US Treasury to manufacture a coin (platinum was suggested, but it could just as well have been made out of gingerbread) and stipulate it to be worth a trillion dollars. Instantly, the Federal government would have an additional trillion dollars to spend, though Congress would have to approve any such spending.

The purpose was to evade irrational limits on the public debt embodied in law. Exceeding these limits would otherwise have depended on agreement by a Republican Congress. The inflationary impact of seigniorage, whether in the form of electronic checks or a zillion-dollar coin, depends on what sort of spending would result, among other factors.

We have enumerated a variety of uses for taxes, but the indisputable, preeminent use is to pay for public spending, or to service the debts incurred to finance public spending. While seigniorage can provide a push, especially during a downturn, at the end of the day, any very large, permanent nondefense spending increase, particularly under Scenarios II or III, will have to be partially offset by a combination of tax revenue, defense cuts, and borrowed funds. The tax-like alternatives discussed above do not necessarily thrive politically. There is no tricky way around reducing private spending to make room for public spending.

In a Technical Appendix, below, we add some numerical detail to the framework proposed here. The objective is not to pretend to provide precise quantitative estimates of the relevant factors, but to indicate the order of magnitude, or the scale of what is in question.

To a great extent, progressive advocacy of expanded public nondefense spending has been supported by the crutch of promises to tax the rich. The new crutch in some MMT punditry is money printing. There has been the promise of an employment boost. By now, a more indulgent attitude towards higher deficits has also settled in. In all of these cases, the benefits of the spending itself for ordinary people tends to be glossed over.

If the public was convinced of the benefits of new spending, financing would be more of an afterthought. As one of Franklin D. Roosevelt’s top advisers, Harry Hopkins, said, “We shall tax and tax, spend and spend, and elect and elect.”

From an economic standpoint, there remains significant potential for nondefense public spending to expand.

Nondefense spending increases may be facilitated by a variety of devices. The greater political obstacle for such increases, other than aversion to taxes, is skepticism that the new programs will bring benefits worth the cost. The real secret to expanding the US public sector, including any Green New Deal and expanded care infrastructure, is to demonstrate the benefits of the spending itself, in its own right.

Seigniorage can provide a boost to public spending, but within limits that are commonly overstated.

Transforming the US public sector along social democratic lines, including implementation of the Green New Deal, will require mass taxation, as it typically does in Europe. In the Technical Appendix that follows, we try to show that seigniorage, defense cuts, and taxation of corporations and the rich will be helpful, but insufficient for this project.

Al Jazeera, “More than 70,000 killed in Yemen’s civil war: ACLED,” April 19, 2019. https://www.aljazeera.com/news/2019/4/19/more-than-70000-killed-in-yemens-civil-war-acled

Ali, Idrees, and Mike Stone, “Pentagon Fails Its First Ever Audit, Official Says,” Reuters, November 15, 2018. https://www.reuters.com/article/us-usa-pentagon-audit/pentagon-fails-its-first-ever-audit-official-says-idUSKCN1NK2MC

Baker, Dean, “HR 1384 —Medicare for All Act of 2019,” Testimony before U.S. House of Representatives Rules Committee on Medicare For All, April 30, 2019. https://www.cepr.net/dean-baker-s-testimony-to-the-house-rules-committe-on-the-medicare-for-all-act-of-2019/

Baker, Dean, “The Gamestop Game and Financial Transactions Taxes,” Center for Economic and Policy Research, January 29, 2021. https://cepr.net/the-gamestop-game-and-financial-transactions-taxes/

Bandow, Doug, “Beto Needs to Revive Talk about His ‘War Tax’ Proposal,” The Cato Institute, September 18, 2019. https://www.cato.org/publications/commentary/beto-needs-revive-talk-about-war-tax-proposal

Board of Trustees, Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds. The 2020 Annual Report of the Board of Trustees, Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, April 22, 2020.

Congressional Budget Office, “Options for Reducing the Deficit, 2021 to 2030,” December 9, 2020. https://www.cbo.gov/budget-options/56846

Furman, Jason, and Wilson Powell III, “What the US GDP Data Tell Us About 2020,” Peterson Institute for International Economics, January 28, 2021. https://www.piie.com/blogs/realtime-economic-issues-watch/what-us-gdp-data-tell-us-about-2020

Gomez, Eric, Christopher A. Preble, Lauren Sander, and Brandon Valeriano, “Building a Modern Military: The Force Meets Geopolitical Realities,” Cato Institute, May 26, 2020. https://www.cato.org/publications/white-paper/building-modern-military-force-meets-geopolitical-realities

Henwood, Doug. Wall Street, Verso, 1997. https://www.leftbusinessobserver.com/WSDownload.html

Hersh, Adam S., and Mark Paul, “How Much Emergency Relief Will It Take to Revive the U.S. Economy?” Groundwork Collaborative, December 8, 2020. https://groundworkcollaborative.org/resource/how-much-emergency-relief-will-it-take-to-revive-the-us-economy/

Holden, Emily, and Laura Gambino, “Sanders to unveil $16tn climate plan, far more aggressive than rivals’ proposals,” The Guardian, August 22, 2019. https://www.theguardian.com/us-news/2019/aug/22/bernie-sanders-climate-change-plan

Internal Revenue Service, “Tax Gap Estimates for Years 2011-2013.” https://www.irs.gov/newsroom/the-tax-gap

Kelton, Stephanie. The Deficit Myth: Modern Monetary Theory and the Birth of the Peoples Economy, Public Affairs, 2020.

Lindorff, David, “EXCLUSIVE: The Pentagon’s Massive Accounting Fraud Exposed,” The Nation, November 27, 2018. https://www.thenation.com/article/archive/pentagon-audit-budget-fraud/

Mitchell, William, L. Randall Wray, and Marvin Watts. Macroeconomics, Red Globe Press, 2019.

National Priorities Project, “Overseas Contingency Operations: The Pentagon Slush Fund.” https://www.nationalpriorities.org/campaigns/overseas-contingency-operations/

National War Tax Resistance Coordinating Committee, “An International History of War Tax Resistance.” https://nwtrcc.org/war-tax-resistance-resources/international-history-of-war-tax-resistance/

Nersisyan, Yeva, and L. Randall Wray, “How to Pay for the Green New Deal,” Levy Economics Institute of Bard College, Working Paper No. 931, May 2019. http://www.levyinstitute.org/publications/how-to-pay-for-the-green-new-deal

Nersisyan, Yeva, and L. Randall Wray, “Can We Afford the Green New Deal?” Levy Economics Institute of Bard College, No. 148, 2020. http://www.levyinstitute.org/pubs/ppb_148.pdf

OECD, “General government spending,” 2019. https://data.oecd.org/gga/general-government-spending.htm

Office of Management and Budget, Budget of the United States Government, Analytical Perspectives, Fiscal Year 2021. https://www.govinfo.gov/content/pkg/BUDGET-2021-PER/pdf/BUDGET-2021-PER.pdf

Paul, Mark, Anders Fremstad, and J.W. Mason, “Decarbonizing the U.S. Economy: Pathways toward a Green New Deal,” Roosevelt Institute, June 2019. https://rooseveltinstitute.org/publications/decarbonizing-us-economy-toward-a-green-new-deal/

Petroff, Alanna, Ivory Sherman, and Tal Yellin, “These are America’s top trading partners,” CNN Money. https://money.cnn.com/interactive/news/economy/how-us-trade-stacks-up/index.html

The Revolving Door Project. https://therevolvingdoorproject.org/

The Revolving Door Project, “Tell President Biden to Keep Corporate Insiders Out of Your Administration.” https://nocorporatecabinet.com/

Sawicky, Max B. (ed). Bridging the Tax Gap: Addressing the Crisis in Tax Administration. Economic Policy Institute, 2006.

Sawicky, Max B., “No Go,” Jacobin, January 3, 2019. https://www.jacobinmag.com/2019/01/no-go

Spoehr, Thomas, “The Pentagon Auditing Process Is Expensive, Inefficient, and In Arrears,” The Heritage Foundation, December 2, 2019. https://www.heritage.org/defense/commentary/the-pentagon-auditing-process-expensive-inefficient-and-arrears

Tax Policy Center, “How do US corporate income tax rates and revenues compare with other countries’?” Urban Institute Tax Policy Center Briefing Book. https://www.taxpolicycenter.org/briefing-book/how-do-us-corporate-income-tax-rates-and-revenues-compare-other-countries

U.S. Department of Defense, “Summary of the 2018 National Defense Strategy of the United States.” https://dod.defense.gov/Portals/1/Documents/pubs/2018-National-Defense-Strategy-Summary.pdf

U.S. Government Accountability Office, “Defense Contracting: DOD’s Use of Competitive Procedures,” GAO-15-484R, May 1, 2015. https://www.gao.gov/products/GAO-15-484R

U.S. Government Accountability Office, “Defense Contracting: DOD Should Clarify Criteria for Using Lowest Price Technically Acceptable Process,” GAO-19-54, November 13, 2018. https://www.gao.gov/products/GAO-19-54

U.S. Government Accountability Office, “Defense Contracting: DOD Needs Better Information on Incentive Outcomes,” GAO-17-291, July 11, 2017. https://www.gao.gov/products/GAO-17-291

U.S. Government Accountability Office, “Corporate Income Tax: Most Large Profitable U.S. Corporations Paid Tax, But Effective Taxes Differed Significantly from the Statutory Rate,” GAO-16-363, March 17, 2016. https://www.gao.gov/products/GAO-16-363

Wistar, Aaron, “Mainstreaming MMT,” LA Review of Books, October 8, 2020. https://lareviewofbooks.org/article/mainstreaming-mmt/

A properly done, detailed budget blueprint would be a huge undertaking. For the purposes of this paper, we provide some rough calculations to provide the reader with a sense of the scale of key sources for new, nondefense public spending under our three scenarios.

Step One. Our first priority is to increase Federal spending sufficiently to move the economy to its full potential. We refer to data for 2019 to set a baseline representing a relatively normal year, compared to the deep recession-plus-pandemic year of 2020.

US GDP was $21.7 trillion in the fourth quarter of 2019. Between 2010 and 2019, annual average growth in GDP, from fourth quarter to fourth quarter, was 3.6 percent. If the pandemic had never happened, it is reasonable to expect that by the end of 2020, GDP could have grown to about $22.5 trillion. The most recent figure for the fourth quarter of 2020 is $21.5 trillion. In and of itself, that suggests a shortfall of a trillion dollars.

By conventional reckoning of the US economy, 2019 was a year of relatively tight labor markets and close to full employment. Was it the best we could have expected? By some analyses, 2019 still left a lot to be desired. While the unemployment rate hit historically low levels, that rate fails to reflect those who have left the labor force but would prefer to stay employed. The labor force participation rate and employment-population rates have been higher in recent decades. One tip-off to the weakness of the labor market has been the anemic growth in wages.

Hersh and Paul note that some states took as much as seven or eight years to return to 2008 levels of economic output.5 Others have yet to recover. They calculate that if the labor force participation rate was at 2007 levels, the official unemployment rate would be 13 percent, rather than 6.9 percent. Paul, Fremstad, and Mason note that by 2019, GDP was 15 percent below the level forecast 10 years earlier.6 Their conclusion is that the Federal government and the Federal Reserve failed in the mission to maximize employment without excessive inflation.

Furman and Powell, no friends of MMT, estimated a current output gap of 5 percent, which is huge.7 Hersh and Paul saw an output gap of $4.5 trillion. (These authors might alter their estimates in light of more recent data.)

From any of these standpoints, as of February 2021, the economy is currently well situated for a burst of money printing and deficit spending, at least for the year to come, and perhaps longer.

A jump to full employment implies a large increase that we should not expect to be sustainable. In other words, if the output gap is 5 percent, policy eliminates it, and the economy stays at full employment. That does not mean that going forward, the annual growth can stay at 5 percent. The causes of economic growth in the long run are poorly understood by economists.

The Biden Administration has proposed an anti-recession package of $1.9 trillion, which is in Furman’s ballpark. It should not be an eye-popping, inflationary number, for at least five reasons.

First, not all of the money will be spent in 2020. Some spending will be delayed. Second, some of the money will be devoted to savings. Families will reduce credit card balances, state and local governments will replenish their reserve funds. Third, the output gap is routinely underestimated. Full-employment GDP could be higher than we think. Fourth, some of the components in the package are onetime expenditures rather than ongoing programs, which reduces any inflationary impact. Other expenditures (raised unemployment benefits) would be expected to shrink as the economy recovers. Fifth, somewhat extra inflation (current levels being exceedingly low) would be less of a risk than too little of an economic recovery.

A contrary view is that the “output gap” in 2019 was actually positive, meaning actual GDP exceeded “potential” or full-employment GDP. A positive gap is taken as a signal of inflationary pressure, though little inflation was in view in 2019. Economists sympathetic to MMT tend to see a greater potential for economic growth (large, negative output gaps), and this writer tends to believe them.

If we grant the merits of increased deficit spending to achieve full employment, it must remain the case that the entirety of the increase will not be green. If we put people to work manufacturing solar panels, they will use their wages to buy hamburgers and televisions. For a GND, a permanent change in the composition of GDP will be required. Our Step One is unlikely to be sufficient in that respect.

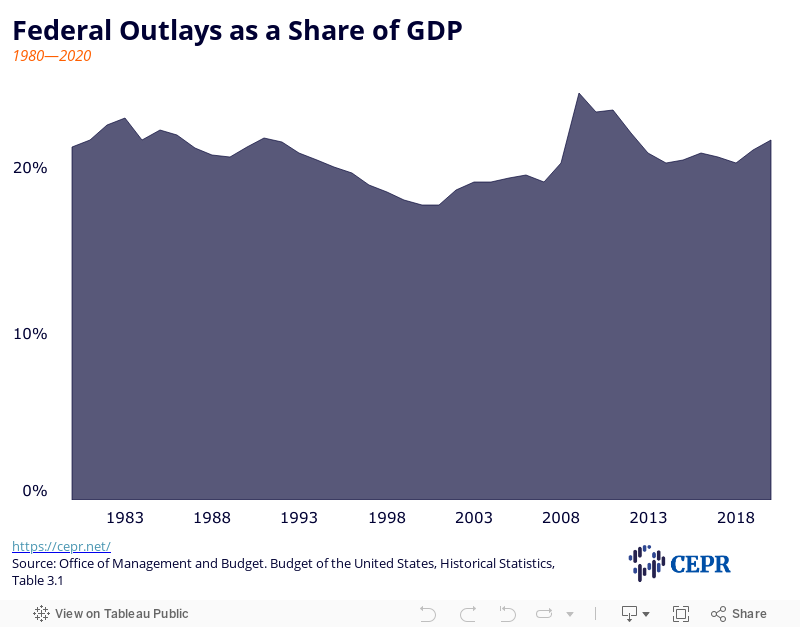

Step Two is a significant expansion, by conventional standards, from the old normal to a new normal. In Fiscal Year 2019 (ending in September 2019), Federal outlays as a share of GDP were 21 percent. Figure 2 shows Federal outlays as shares of GDP from 1980 to 2020. We suggest a significant increase that is not far out of line with recent experience would take the Federal government up to 24 percent of GDP. (As mentioned before, the nondefense increase can be greater, insofar as defense spending is reduced.) With respect to 2019 GDP, an extra 3 percent devoted to Federal spending would have been $650 billion, about a 15 percent increase in the Federal budget.

Step Two is defined here as a significant but limited, permanent increase in Federal spending from a base of high employment. In this case, more Federal nondefense spending must mean less of something else. Seigniorage and deficit spending can’t work. At full employment, money printing and increased deficit spending are inflationary. Some combination of defense cuts and tax increases will be required.

As noted above, in 2019 3 percent of GDP in 2019 would have been $650 billion. The defense budget was about $686 billion. Zeroing out defense would just cover the increase, which of course is totally unlikely. Taxes would have had to make up the difference.

Step Three is a transition to a social democratic system. Going by data from the Organisation for Economic Co-operation and Development, total US Federal, state, and local public spending was 38 percent of GDP. Of course, the likelihood of the Biden Administration going down this road is remote, but as shown below, it might be essential for a GND. Social democratic nations of Europe spent in the range of 40 to 56 percent of GDP in 2019. If we take these as tenable, admittedly very ambitious models for the US, we might set a goal of a permanent net increase in US public spending of 10 percent of GDP.

A review of GND plans by Nersisyan and Wray found they averaged close to 5 percent of GDP, so a 10 percent increase would cover GND policies and leave much for other needs.8 If limited to a 3 percent of GDP increase in nondefense spending, a GND might be a tight squeeze.

Under conditions of higher employment, such as existed in 2019, it is easier to hypothesize a 10 percent expansion of public nondefense spending than it is to specify plausible tax increases and spending cuts that would make that possible. Again, with reference to 2019, where would $2.2 trillion have come from? We are again assuming a base of full employment. Under full employment, a public sector expansion must mean a private sector contraction. The composition of GDP changes, not its level or rate of growth.

One important mitigating factor is the extent to which the change in composition brings improvements in efficiency. A leading possibility in this respect is health care.9 The bloat in the US system, revealed by comparison to public systems in other nations of equal or superior quality, presents an opportunity to increase useful GDP output.

We have already seen that defense spending would not be sufficient, even under Step Two. Even if half of the $686 billion was carved out, we would still be a long way from $2.2 trillion.

Another progressive priority is taxing the rich and corporations. How much potential is there? Taking corporations first, in 2019 total corporate profits were $1.8 trillion, of which $312 billion was already collected in taxes. Here again, another 20 or 30 percent, a huge increase by historic standards, still leaves us a long way off.

For additional taxes on the rich, we have to look to the income of unincorporated business firms, which is roughly double that of corporate income. Here, however, we are talking about taxpayers with wide disparities in the ability to pay, from mom and pop bodegas and landlords (many crippled now by the recession), to the likes of partners in well-heeled law firms and other partnerships. Their income is only accessible through the individual income tax.

A possible exception is the legal status of “S-corps,” which could be abolished; the affected taxpayers could then be required to pay more because their ownership interest would be taxed first at the firm level, under the corporate income tax, and again at the individual level, under the individual income tax. This has been the status quo for those with ownership interests in “C-corps” (e.g., shareholders) that have been required to file under the corporate income tax.

We noted above that a percentage point increase in the top two marginal tax brackets brought in $114 billion, over 10 years. We also cited work suggesting much greater increases were possible. In the present context, however, a tenfold increase that only gets $114 billion a year pales in comparison to our goal of $2 trillion annually. An increase in taxes on capital gains is the same order of magnitude. Such tax increases would promote after-tax income equality, but they are not plausible sources of a greatly and permanently expanded public sector.

What about tax expenditures? A great part of them derives from itemized deductions in the individual income tax. Eliminating all itemized deductions, according to the Congressional Budget Office, gains $1.7 trillion over 10 years, or $170 billion a year. The payroll tax is the second greatest source of Federal revenue. Here a percentage point change in the rate gets $800 or $900 billion, again over 10 years, and it should not be forgotten that increased tax revenue from some source will be needed for Social Security and Medicare.

One of the biggest revenue raisers catalogued by CBO is a value-added tax (VAT), which is similar to a sales tax. A 5 percent tax on a broad base is estimated to bring in $2.8 trillion over 10 years. In the same vein, a tax on greenhouse gas emissions gets about $1 trillion over 10 years. In light of the undesirable distributional impact of such taxes, the need for a substantial rebate for lower-income taxpayers would significantly reduce the net revenues obtained. For our Scenario III, we would probably be looking at a VAT rate of 15 percent.

The same cautionary note provided with regard to tax expenditures applies here. The whole of a large tax revenue increase will be less than the sum of its parts. Increased revenues for multiple provisions will overlap to some extent. This also applies in a political sense. Higher taxes in one area elevate political opposition to increases in other areas.

The bottom line is that plausible, large tax increases on corporations and the rich, combined with a large defense cut, can get us to Scenario II, but not to Scenario III. For Step Three, tax increases on the middle class, broadly defined, will be required, and such increases will be rejected without a persuasive case for the spending that would be made possible.

As Nersisyan and Wray say, the source of resources for a GND are derived from “a combination of shifting them from other uses and moving them from unemployment (broadly defined — that is, not limited to the official measures of unemployment).”10 They also acknowledge, “It is possible that we will need to constrain domestic consumption in order to release resources for the GND effort in a noninflationary manner.”

Moving resources “away from unemployment” (closing the GDP gap) corresponds to our Step One above. With Wray, we agree that the gap to be closed is probably larger than conventionally imagined. Shifting from other uses means shifting from defense to nondefense, or shifting from the private to the public sector. The latter requires taxes or what we have characterized as “tax-like” substitutes. In all cases, the point is to infuse new spending with GND guidance.

As noted above, a review of GND plans by Nersisyan and Wray found they averaged close to 5 percent of GDP, which could prove to exceed the GND spending absorbed by reaching full employment, or by going beyond that as in Scenario II.11

Senator Bernie Sanders’s plan had a price tag of $16.3 trillion, spread over 10 years. Governor Jay Inslee of Washington state offered a plan costing $9 trillion. One percent of the 2020 GDP that might-have-been ($22.5 trillion, as above) is $225 billion. Inslee’s lower number is close to 4 percent of GDP ($900 billion divided by $225 billion, with some allowance for less than $225 at the start of 10 years and more going forward).

A 10 percent increase in Federal outlays would cover GND policies and leave much for other needs. Scenario II, with increases of 3 or 4 percent of GDP, would be a tight fit, especially if it is granted that the GND must be a New Deal that is green. Any such increase in nondefense spending would be beset with demands for a variety of worthy causes. First among them might be universal health insurance coverage. The rising costs of Social Security, compared to slower growth in payroll tax revenue, will also weigh on prospective revenue increases in the future.

The awful truth is that what we want requires social democracy, and social democracy requires mass taxation, quite possibly based on a new, national value-added tax.