July 17, 2015

Mark Weisbrot

Al Jazeera America, July 17, 2015

Público, August 7, 2015

View article at original source.

The battle over the future of Europe – currently centered in Greece – is far from over. But, with the tentative deal that has been struck between the Syriza government and European authorities, it has certainly entered a new phase.

Prior to the July 5 referendum, European officials had been carrying out a strategy of “regime change.” Deadlines came and went, and threats of a forced Grexit were mainly bluff, despite the fact that the most powerful leader of the eurogroup of finance ministers, Germany’s Wolfgang Schäuble, seemed to favor it. The strategy of regime change looked relatively easy: the European Central Bank (ECB), by restricting credit, together with the standoff and rumors of Grexit, had already pushed the Greek economy back into recession. It seemed only a matter of time before the economic failure, combined with anti-Syriza media coverage, would undermine support for the Greek government enough to usher in a new one.

In his first interview since his July 6 resignation from the post of Greek finance minister, Yanis Varoufakis describes “The complete lack of any democratic scruples, on behalf of the supposed defenders of Europe’s democracy,” i.e., his eurozone negotiating partners. They continuously “delayed and then came up with the kind of proposal you present to another side when you don’t want an agreement.”

On June 26, Greek Prime Minister Alexis Tsipras called their bluff by announcing the referendum, which on July 5 produced a landslide “no” vote against further austerity and regressive “reforms.” This made regime change a somewhat more cumbersome strategy: If you are going to get rid of a government by wrecking the economy, the people have to blame the government rather than the officials who are wrecking the economy. But the vote showed that Greeks saw who was responsible for their misery, especially after the ECB, in an effort to intimidate voters, forced a closure of the banking system – something it had not done in the past six years of crisis and depression.

This strengthened the position within the European camp of Schäuble and his allies who favored an “out now” solution. Tsipras was faced with a choice, it appears: to accept the European authorities’ terms, or be forced out of the euro as the ECB continued to destroy the Greek banks and financial system. It was a hostage situation. He chose to surrender, defending his decision on the grounds that although the voters had clearly rejected austerity, they also did not want to leave the euro.

But the current deal, if it holds, almost certainly will not allow for the Greek economy to recover. The primary budget surplus targets of 2, 3, and 3.5 percent of GDP for the three years of the deal, 2016 through 2018, will make sure of that, given that the country is running a primary budget deficit right now. Of course, the government is unlikely to be able to meet these targets as the economy and therefore government revenues shrink. The Financial Times estimates that primary surpluses will contribute just 4.5 billion euros over the three years. Even if this estimate turns out to be low, this is a small part of a package currently estimated at 86 billion euros.

The fact that European officials are willing to keep the Greek economy indefinitely stuck in a depression for such a small fraction of the money that they are putting up – really pocket change relative to their resources – should be an eye-opener for anyone who is following the drama. It means that the European authorities are really not interested in an economic recovery in Greece in the near future. It also indicates that this fight is not mostly about the debt itself, but part of a much larger political struggle over what kind of society Greeks (and tens of millions of other Europeans) will live in.

The European authorities have now made it clear that – so long as they are in control of Greece’s economic policy – the country’s depression and mass unemployment will continue indefinitely.

Even further debt relief, which is not yet part of the deal, will not improve the situation over the next three years, since it is very unlikely to reduce interest payments during this period.

So what can be done? In his post-exit interview, Varoufakis describes three steps that he advocated in response to the ECB forcing the closure of Greek banks:

We should issue our own IOUs, or even at least announce that we’re going to issue our own euro-denominated liquidity; we should haircut the Greek 2012 bonds that the ECB held, or announce we were going to do it; and we should take control of the Bank of Greece [the Greek central bank].

These were steps in the direction of leaving the euro, but not irreversible ones. They were moves that would help prepare the government to keep the economy functioning in the absence of an agreement with the creditors. They would also show that Greece was not completely at the creditors’ mercy.

But Varoufakis was outvoted, he said. He also noted that although there was a small team that had worked on the details of an exit from the euro, “To prepare the country an executive decision had to be taken, and that decision was never taken.”

Such preparation would now appear to be prudent, since the masks have come off and the whole world can see how mean and ruthless the current leadership of the eurozone is willing to be in order to impose their own brand of economic order on the common currency area. If Greece left the euro, things would likely get worse before they got better, but the economy would recover.

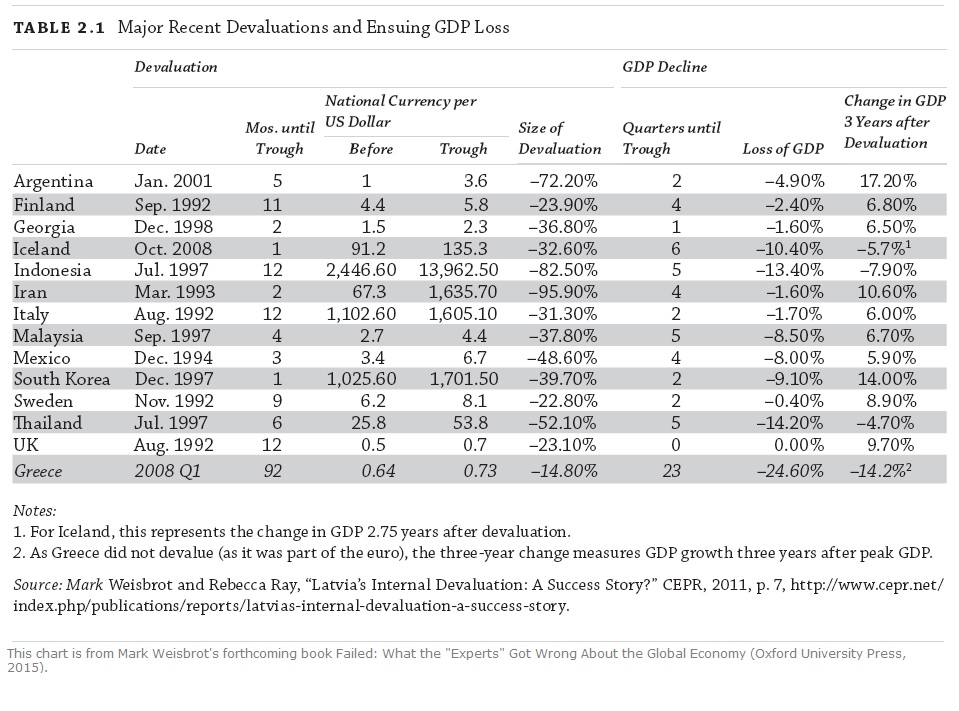

As is well known, Argentina suffered a very severe financial crisis after it defaulted on its debt at the end of 2001 and de-linked its currency from the dollar in January of 2002. However, the economy was growing three months later, and went on to grow 63 percent over the ensuing six years – one of the fastest rates of growth [PDF] in the world during this period. Contrary to popular belief, growth was not driven by a “commodities boom” nor by exports. Although Greece has more exports as a percent of GDP than Argentina did, and would benefit from a devaluation, the main boost to recovery – as in Argentina – would come from being able to escape from the destructive economic policies imposed by foreigners. (Argentina had just one-third of the troika to deal with – the IMF – but it was a pretty deadly constraint.)

Some economists have correctly noted that a default and devaluation that involves creating a new currency presents additional challenges, as compared with Argentina’s abandoning the peso/dollar peg. But this does not change the basic story. A developed economy does not transform itself overnight into a failed state, simply because it exits from a currency union. We can look at the worst financial crises over the past 25 years, and none of them resulted in the kind of economic damage that Greece has already suffered. It is not clear why anyone would argue that Greece would be worse off leaving the euro than it would be three years from now if it were to follow the economic program that it is currently finalizing with the European authorities.

Meanwhile, despite the unconditional surrender of the Syriza government and the parliament’s approval of the hated austerity measures that the European authorities demanded, the ECB did not increase its Emergency Liquidity Assistance to Greek banks so that they could open. The banks remain closed today (Thursday). The ECB appears to be in no hurry to let up on the accelerated economic damage that it has been deliberately inflicting on the Greek economy over the past few weeks in order to force this agreement.

Mark Weisbrot is co-director of the Center for Economic and Policy Research in Washington, D.C. and president of Just Foreign Policy. He is also the author of the forthcoming book “Failed: What the ‘Experts’ Got Wrong about the Global Economy.“

{kind=link}